Citation

Oliver, J.J. (2016), "Benchmarking workforce productivity in the creative industries", Strategic HR Review, Vol. 15 No. 1. https://doi.org/10.1108/SHR-10-2015-0082

Publisher

:Emerald Group Publishing Limited

Benchmarking workforce productivity in the creative industries

Article Type: Strategic commentary From: Strategic HR Review, Volume 15, Issue 1

John J. Oliver

John J. Oliver is Associate Professor at Bournemouth University, Bournemouth, UK.

Overview

The competitive dynamics of many industries have changed considerably over the past decade and perhaps none more so than in publishing. There is no doubt that this industry continues to undergo structural changes that compel businesses to adapt and transform themselves to the demands and disruption caused by innovative new media technologies. But how has the workforce responded to these dynamic changes and what has been the impact on industry performance? This paper presents the findings from a comparative time-series analysis (1997-2013) of the UK Publishing Industry and compares it to other industries categorised within the UK Creative Industries. In doing so, it extends our understanding of inter-industry workforce performance and provides an insight into how the UK Publishing Industry has adapted to digital media over two decades change and turbulence.

Creative destruction and innovation

There is no doubt that the UK’s Creative Industries have been one of the economic successes of the past generation. Firms within these industries have increased their contribution to the UK economy from £31,205 million in 1997 to £76,909 million by 2013. The size of the workforce has also significantly increased from 931,000 employees in 1997 to 1,708,000 in 2013.

This optimistic economic picture is not replicated in the Publishing Industry where a substantial number of job losses have reduced the number of employees from 308,500 in 1997 to 231,000 in 2013. If ever one wanted to paint a picture of the creative destruction caused by innovative new technologies on an industry, then we need not look any further than publishing.

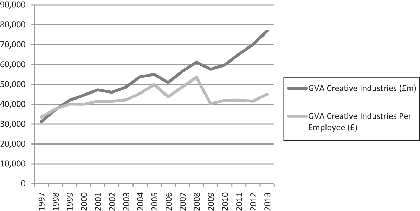

Discussions on the UK economy, from a number of political and economic sources, have centred on the issue of high levels of employment, but relatively low levels of productivity following the Global Financial Crisis of 2007-2011. Indeed, this question is equally relevant to the Creative Industries, where Gross Value Added (GVA) per Employee has yet to recover from the peak of £53,542 in 2008. Whilst there has been a strong recovery in Total GVA and the number of employees between 2009 and 2013, at 33 per cent and 19 per cent, respectively, the GVA per Employee has only increased by 12 per cent over the same period. In essence, this trend equates to a productivity gap within the Creative Industries that has been sustained between 2009 and 2013 (Figure 1). Whilst productivity gaps tend to be discussed in terms of output per employee between one country and another, it is not unreasonable to consider it in terms of industry and inter-industry analysis, particularly when considering the use of benchmarking to evaluate human resource performance levels. In many ways, these lower levels of GVA per Employee and concerns over productivity are to be expected, as the sustained harshness of macro-economic conditions, created by the Global Financial Crisis, will have affected business capital expenditure, investment in research and development, skills training and a lack of competition in the market place.

Figure 1 - Creative industries: GVA and GVA per Employee

Benchmarking and inter-industry workforce productivity

The strategic adaptation and renewal of resources at industry level, is perhaps, most visibly demonstrated in the structural changes of the workforce. The UK Publishing Industry illustrates these changes more than any other with significant job losses as a result of extraordinary changes in the macro-environment. These include: the collapse of the dot.com economy in 2000 which resulted in 33,100 job losses; the disruption caused by new media technologies in 2004 which resulted in −30,900 job losses; and the initial effects of the Global Financial Crisis which resulted in 33,100 job losses in 2008.

Whilst there have been job gains following these events (+9,400 in 2001; +18,400 in 2003; +16,400 in 2006; and +19,000 in 2012), the net number of job losses between 1997 and 2013 equates to an astonishing 77,500.

However, this strategic adaption of human resources has delivered superior performance in terms of productivity. Whilst the human cost of these job losses is incalculable, from an economic point of view, the long-term reduction in the workforce has delivered vastly improved results in terms of productivity within the Publishing Industry. Figure 2 below illustrates the inter-industry GVA per Employee performance based on comparative figures for the year ending 1997-2013. Here, we clearly see that the Publishing Industry has by far outperformed any other industry, by increasing the GVA per Employee from £20,554 to £43,022 (+109 per cent). The next best performance is seen in the Architecture Industry which has increased GVA per Employee from £14,530 to £26, 412 (82 per cent) and IT, Software and Computer Services where GVA per Employee increased from £25,952 to £42,513 (64 per cent). The worst performing industry was Film, TV, Video and Radio where GVA increased by 56 per cent, from £5,985 m to £9,308 m and the number of employees increased 60 per cent, from 161,800 to 259,000. The result was a net reduction in GVA per Employee of −3 per cent, from £36,990 to £35, 938.

Figure 2 - Inter-industry GVA per Employee performance (1997 and 2013)

What these figures indicate is that at two points in time, 1997 and 2013, the GVA per Employee performance in publishing has by far exceeded peer creative industries. In all instances, with the exception of publishing, the number of employees in each industry increased between 1997 and 2013. In effect, the increasing Publishing Industry GVA and decreasing number of employees have produced an adaptation in the industry and the workforce that has resulted in far higher levels of productivity in comparison to peer industries.

Conclusions

The UK’s Creative Industries provide an ideal context to examine a transformative environment, driven by increasingly innovative digital technologies. As a whole, these industries have increased their human resources significantly, and yet this investment has led to varying degrees of success in terms of productivity. On the positive side, we have Total GVA for all creative industries increasing on an annual basis and GVA per Employee rising significantly between 1997 and 2013. However, GVA per Employee peaked in 2008, and whilst there has been significant investment in human resources in the form of the number of employees, the return on this investment has not yielded significant increases in GVA per Employee. So much so, that the data presents a strong argument for weak performance levels in terms of workforce productivity.

In terms of how the UK Publishing Industry has performed over time, we see a structural adaption of human resources which, perhaps surprisingly, have produced positive effects on workforce productivity. For example, whilst the industry has contracted in terms the number of employees, this reconfiguration of human resource has resulted in a far more productive workforce.

About the author

John J. Oliver is Associate Professor of Media Management and experienced academic-consultant whose work has been published in international business and management journals. He is also a Visiting Fellow at the Reuter’s Institute for the Study of Journalism at the University of Oxford. John J.Oliver can be contacted at: mailto:joliver@bournemouth.ac.uk