Citation

French, N. (2008), "The valuation of rack rented freehold property", Journal of Property Investment & Finance, Vol. 26 No. 2. https://doi.org/10.1108/jpif.2008.11226bab.001

Publisher

:Emerald Group Publishing Limited

Copyright © 2008, Emerald Group Publishing Limited

The valuation of rack rented freehold property

The valuation of rack rented freehold property

1 Reversionary properties

A reversionary property is one that has a cash flow that starts between rent reviews or where the lease pattern is irregular. In simple terms, the initial rent will be received for a period of time that is different (normally less) than the normal market rent review length.

2 Introduction

In the previous articles in this series, I looked at the valuation of rack-rented property by implicit and explicit methods. The following is an expansion of the two approaches to value properties that are let at a rent above or below the current market rent (MR). These are known as reversionary freehold properties. With the valuation of rack rented property, it was shown that a discounted cash flow (DCF) explicit valuation produces an identical valuation to the all-risk yield (ARY) implicit approach. The conventional method implicitly mirrors the explicit assumptions of the DCF valuation. The implicit method can therefore be viewed as a short cut to the DCF.

As previously stated, “the yield or capitalisation rate” in the implicit valuation includes implicit assumptions about risk and growth. The “market” capitalisation rate will relate to a comparable property on a “normal” rent review pattern (every five years), the growth implied in that capitalisation rate being dependent upon that rent review pattern. Thus if the property to be valued is to be let at MR on the same rent review pattern, it is perfectly correct to use the ARY from the comparable. However this is only true for properties let at Market Rent (MR). In the case of properties let at below (or above) MR the implicit method does not produce the same answer as the DCF, nor is it rational in its approach. For the sake of illustration this article will concentrate on examples where rentals are currently below MR and where rents are rising. The next article will discuss the problems of valuing properties in a falling market where a significant degree of overage or over-renting is being experienced.

3 Reversionary freeholds

A reversionary freehold is simply a property where the rent passing is below (or above) MR. There will therefore be a reversion at a future date when MR will be achievable, either at rent review or lease renewal. The valuation is considered in two stages:

- 1.

The term. The period for which the current income is fixed.

- 2.

The reversion. the period following the expiry of current rent.

Of course, in reality, any property has a series of reversions when it is hoped that the rental will increase. Property is an investment that over the long term has always been perceived to benefit from growth. Indeed rent reviews were introduced in the 1950s and 1960s to allow the investor to benefit from the inflationary pressures in the economy. Rents are therefore expected to change, say, every five years depending on the rent review period.

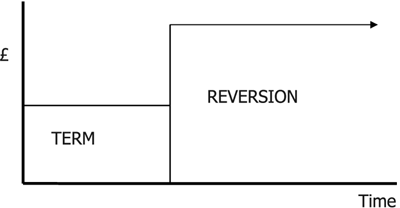

However, traditionally, the valuer has only been concerned with the first reversion when MR is achievable. The reason for this is that, as with the conventional valuation of a rack rented freehold, there is a resistance by the valuer to make any explicit assumptions as to rental values in the future. Thus in the implicit valuation of a reversionary freehold all rentals are expressed in current day terms and any growth that is expected will be implied by the capitalisation rate. There are, however, a number different methods for valuing this interest. Where a property is currently let below MR (either between rent reviews or on the remainder of an existing lease), and where it is expected for that income to increase to MR at a future date, then the investment is known as a reversionary interest. Traditionally, two methods of valuation are suggested as possible methods of approach; the implicit term and reversion (using both variable and equivalent yields) and the layer method[1]. The first of these methods view the income flow in two sections; the finite term and the perpetual reversion. This can be represented diagrammatically as shown in Figure 1.

However, if, instead of viewing the reversion as a completely new income flow, the reversionary income is viewed as a continuation of, and an increase to, the term income, then the diagrammatic cash flow changes, as shown in Figure 2.

4 Implicit term and reversion

As with the implicit valuation of freehold property rack rented at MR, this method incorporates all its growth assumptions within the capitalisation rate. Thus in considering the income receivable on reversion (the reversionary income) growth is ignored, since it is reflected in the low capitalisation rate. This is illustrated in Figure 3 (1) with the valuation of a property let at £750,000 for the next three years, the current MR is estimated to be £1,000,000. The appropriate all-risk yield derived for similar rack rented properties is 8 per cent. It should be noted that this information builds on the examples presented in the previous articles. It is therefore already noted that the capital value of the rack-rented property today is £12,500,000. The value of this reversionary property will therefore be below this figure. Similarly, assuming that there will be growth in rentals over the next three years, it would be expected that the capital value of the subject property at reversion would be above this figure if investment yields remain constant.

Figure 3 Implicit reversionary valuations

Analysing the valuation it can be seen that whilst the implicit term and reversion valuation (still predominantly used by the profession) in Figure 3 (1) produces an answer of £11,891,140, which as expected is below the £12,500,000 of the rack rented comparable, it achieves this value by an irrational method. Note that the term is valued at 7 per cent (1 per cent below the all risk yield of the comparable to reflect additional security of the term income), this is a low capitalisation rate and thus implies growth in the cash flow for that three year period. Yet there is no growth in the income during the term; it is fixed by the lease. An equivalent government stock for the same period would yield approximately 10 per cent. Thus the valuation is over-valuing the term. The valuation then compensates for the overvaluation of the term by undervaluing the reversion. This is because it keeps the MR figure in current day terms. Yet the assumption within the valuation is that the actual MR in 3 years will have grown to above £1,000,000. As a result the projected capital value of the reversion in 3 years is the same as the rack rented freehold today. This is clearly wrong. The whole valuation is based on two mistakes cancelling each other out such that the summation of the term and reversion still produces a valuation which approximates to “market value”.

A variation on the implicit term and reversion valuation is the equivalent yield valuation where the valuer makes no adjustment to the yield used on the term. The same yield is used throughout the valuation thus the cash flow can be divided either vertically (term and reversion) or horizontally (layer). It can be seen that the valuations in Figure 3 (2) and (3) produce the same figure of £11,855,726, slightly lower than the term and reversion method (above) using differential yields. However, the same criticisms apply to the term and reversion methodology regardless of the use of different or equivalent yields. Both methods use “growth” capitalisation rates on the “fixed” term income; both use “current” MR at the reversion. The layer method makes similar irrational assumptions. The argument for splitting the cash flow horizontally is that the uplift at reversion (top slice) represents an increase above today’s rent and thus the rent passing today can be viewed as a continuing income in perpetuity from today, the top slice as a perpetual income from three years hence. In theory this split is logical as it allows the valuer to treat the top slice as the riskier part of the investment. There is no guarantee that the increase will occur in three years. Conversely, the layer income is viewed to be fixed and continuing in perpetuity and yet the valuation values it at a “growth” capitalisation rate. Again the valuer is implying growth in the part of the cash flow, which by definition is “fixed”. Once again the implicit methodology relies on serendipity to derive “market value”.

5 Modified or short cut discounted cash flow

An alternative to the three implicit methods illustrated above (and a number of variations not shown here) is to correct the “errors” in the term and reversion method. This is illustrated in Figure 4 (1). Here the term rental is valued at the equated yield of 10.75 per cent (Govt Stock rate plus risk – see previous articles) so not to imply any growth. Note that the value of the term is now less than the over-valued term of the implicit method. It is £1,840,785, which is over £100,000 less than the implicit valuation of the same. The overvaluation of the term has been corrected. It is therefore important that the second mistake of the under valuation of the reversion in the implicit valuation is also corrected. This is done by explicitly allowing for growth in MR at review. (£1,000,000×(1.032)^3=£1,099,016). The capital valuation of the reversion is now above the £12,500,000 of the rack-rented freehold today at a figure of £13,737,697. Given the expected growth in the market, the capital value of the reversion should be higher than an equivalent rack-rented freehold on the market today. However, this figure is three years hence and must be discounted back to today. The present value calculation is at the equated yield of 10.75 per cent. It can be seen that in this case the values produced by the two valuations differ quite considerably (£98,122 in favour of the modified DCF method) – but which is the “correct” valuation?

Figure 4 Conventional (DCF) reversionary valuations

If it is accepted that the value of a property investment will be equal to the present value of the income flow (rent) produced by that property, allowing for risk and growth. Then, it can be seen that a full DCF valuation will achieve this objective with all assumptions explicitly stated. Indeed, where a property is let at MR with regular rent reviews, the implicit method was effectively a “short-cut” to the DCF method (both produced the same value), and as such was to be preferred for its brevity. Thus, a full DCF valuation of a reversionary interest will derive that “correct” capital value; this can then be compared with the values produced by the modified DCF method and the implicit term and reversion valuation above.

6 Full discounted cash flow

The basis of a discounted cash flow valuation is that the value of a property investment will be equal to the discounted value of the projected rental income flow, at the investor’s required rate of return (target rate) – the equated yield. This is illustrated in Figure 4 (2) where the valuation is undertaken allowing for three rent reviews before it is assumed that the property is sold in year 14. In this valuation, as with the rack-rented freehold, the method allows for growth (at 3.20 per cent) explicitly at each of the first three reviews and thus discounts the predicted rental figures back at the equated yield of 10.75 per cent. Thereafter it reverts to an implicit valuation and sells the investment in year 14 at the all-risk yield of 8 per cent (YP=12.5). This “sale” figure is then discounted back at the equated yield of 10.75 per cent. It can be seen that the full DCF valuation produces the same value as the modified DCF method at £11,953,848. Thus it can be argued that the implicit term and reversion valuation thus produces an “incorrect” answer. This will be discussed in more depth in the next article.

Nick French

Note1.Note, in practice a number of practitioners will refer to the layer method as the hardcore approach and may make a number of arbitrary adjustments to the yields used on the layer and top slice. These approaches are variations on a theme and the article will simply look at the layer approach as a whole using equivalent yields.2. £1,099,016 × 12.5= £ 13,737,697. This is the capital value of the reversion in three years.3. YP in perp at 8 per cent to allow for implicit growth after the third review