Citation

Abbink, J. (2010), "Optionality", Journal of Risk Finance, Vol. 11 No. 4. https://doi.org/10.1108/jrf.2010.29411daa.001

Publisher

:Emerald Group Publishing Limited

Copyright © 2010, Emerald Group Publishing Limited

Optionality

Article Type: Commentary From: The Journal of Risk Finance, Volume 11, Issue 4

As with many terms that are widely used in finance, particularly those that are bandied about in alternative investment circles, “optionality” has taken on many meanings, to the point that it is not clear that it any longer means much of anything in particular. Promiscuous over-use, notably among fund marketers but also in investment discussions generally, has robbed the concept of much of its definition. This is unfortunate, because optionality is important to the discussion of all types of investments, not just alternative ones, and preserving its sense is of some value. The significance of optionality is that the return distributions of investment techniques that exhibit it cannot be analyzed with any acceptable degree of accuracy by methods that rely on linear regression. These methods support essentially all of the central constructs of modern portfolio theory, notably the capital asset pricing model, arbitrage pricing theory and even (perhaps most surprisingly) option-pricing formulae. So to the degree that optionality is present in investment techniques, much of the financial thinking of the last 50 years is in need of a measure of reconsideration. This paper attempts to recapture some precision for the term.

Use of financial options to model the returns achievable in various investment situations – whether those situations actually involve the use of options or not – is the “cash value” in discussions of optionality. These sorts of analyses have been with us at least since Merton (1981) and the companion paper by Henriksson and Merton (1981), where market timing between long only equities and cash was modeled using a combination of a long position in an index and long positions in put options on that index that have an exercise price that produces a return equivalent to the return on cash. Bookstaber and Jacob (1986, p. 26) noted that corporate credits can be regarded as combinations of treasury securities of comparable duration with a short position in a put option on the issuer’s equity, an analysis that was popularized by Fridson (1994, p. 83), and sparked something of an option-analogue industry. Subsequent studies, including Agarwal and Naik (2004) and Kocagil (2004), among others, extend such analyses to a wide array of assets and trading techniques. A summary of this literature and further analysis can be found in Lhabitant (2004, p. 202ff).

Part of the problem with optionality is that it is a matter of “family resemblances” in the sense that Wittgenstein discussed in some of his later writings: there is no single, core definition but rather a constellation of meanings that together form a somewhat diffuse but nevertheless powerful concept. Perhaps, the best-known example of the challenges in dealing with such concepts was described by Potter Stewart in his concurring opinion to the 1964 US Supreme Court decision in Jacobellis vs Ohio:

I shall not today attempt further to define the kinds of material I understand to be embraced within that shorthand description [of obscenity]; and perhaps I could never succeed in intelligibly doing so.

But I know it when I see it, and the motion picture involved in this case is not that.

We know optionality when we see it, but are likely to be challenged to put a firm definition on it. However, we are not quite as embarrassed in our ability to circumscribe the concept as Justice Stewart was with regard to obscenity. In the case of optionality, the definition revolves around five key elements:

- 1.

asymmetry of returns;

- 2.

bivalence;

- 3.

sensitivity of returns to the volatility of the underlying investment;

- 4.

exercise; and

- 5.

notional leverage.

Not surprisingly, all three are implicit in the standard definition of a financial option as “the right, but not the obligation, to buy (sell) a specified amount of the underlying at a specified price at some specified future date(s),” as well as all of the accepted models for valuing options. I will examine each of these features of optionality in turn.

Asymmetry of returns

Before embarking upon into a discussion of what asymmetrical returns are, it will be useful to indicate what they are not. They are not excess returns, alpha, information efficiency or similar products of superior research, timing prowess or good fortune. They are not an investment product’s performance edge and they are not a feature that is distinctive of, or even unique to, alternative investments generally or “absolute return” vehicles specifically. Much of the confusion that surrounds the concept of optionality is the tendency, especially among fund marketers, to conflate it with one or all of these notions. However, some of the literature that makes use of the concept of optionality tends to foster this confusion. For example, Merton (1981) specifically but unnecessarily associates “successful” market timing with the possession of the options he describes, when in fact all would-be market-timers can be said to hold such options – the “successful” ones distinguish themselves in exercising them in timely fashion rather than in having access to them in the first place.

Symmetry is a binary property of relations – there is no middle ground between symmetry and asymmetry, so there is no sense in which symmetry admits of degrees, except as a function of our units of measurement. If we speak of something, for example, a face, as being “more or less symmetrical,” what is meant is that at a gross level of detail it is symmetrical but at some finer level of detail, says the tilt of an eye or the corner of the mouth, it is not. However, there are degrees of asymmetry – for example, a finger is only slightly asymmetrical compared to a hand, and a hand is less asymmetrical than an arm. Where distributions of returns are under consideration, their degree of asymmetry is measured by their skewness. Skewness is either zero (i.e. the distribution is symmetrical) or it is not, but if it is unequal to zero, skewness (asymmetry) may take any positive or negative real number value. It is this statistical property of return series that exhibits optionality that causes problems for the standard models of finance theory, and the problems increase the more the series’ skewness deviates from zero.

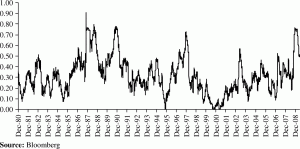

The return distributions of essentially all investable instruments seem to exhibit non-zero skewness, although over short time periods their skewness can be quite variable and may actually have a value of zero, as Figure 1 suggests. The skewness for the 14,878 daily observations that contribute to the series shown in the chart was −0.72, but 11 percent of the 90-day trailing observations were ±0.05, which is close enough to zero as makes no difference, being less than half the standard error of the skewness calculation.

Figure 1 clearly discredits to any claim that asymmetry of returns is a property that is peculiar to alternative investments, but the return asymmetry with which discussions of optionality are generally concerned is greater than the modest positive bias to its returns – median daily return 0.035 percent, mean daily return 0.029 percent – exhibited by the Standard & Poor’s 500 Index for the entire period shown. Return asymmetry is associated with options precisely because of the significant disproportion between the gains and the losses that they offer, depending on the strategy employed. The asymmetry in the returns of broad equity benchmarks may explain the difficulty that dedicated short-sellers have in achieving acceptable returns on a consistent basis, and also their occasional spectacular gains, but it is to the much stronger “hockey stick” asymmetry exhibited by listed option payoff diagrams that discussion of optionality generally refers. For example, over the period from January 1998 to April 2009, monthly returns for the Hedge Fund Research HFRX Merger Arbitrage Index exhibited skewness of −1.21: noticeably higher than that of the Standard & Poor’s 500 Index. This is less a function of the skewness of returns than their bivalence as contingent claims on return streams.

Bivalence

There is in fact a class of exotic options known as binary options – those that pay out a predetermined rather than a variable amount upon exercise – so I have chosen to use the term “bivalent,” although “binary” is probably more correct usage. Although not all options have bivalent payoff structures, those with which investors are most familiar decidedly do. Such an option either exercises or it does not: there is no middle ground. For option buyers, losses are limited to the premium paid and gains are potentially unlimited, while for option writers, gains are limited to the premium received and losses are potentially unlimited. Thus, the asymmetry of their potential payoffs is blindingly obvious. Structures employing two or more traded options in combination may complicate the picture, but the payoff structures of their individual constituents remain bivalent for all that the total structure may offer a different payout profile.

Bivalence characterizes numerous situations encountered in financial markets: a debt issuer defaults or it does not, a merger goes through or it does not, a drug is approved by the Food and Drug Administration or it is not, and so on. However, bivalence need not result from the instrument’s fundamental characteristics but can be a consequence of the trading discipline that is applied to it: for example, the familiar trading desk rule “ride the gainers and cut the losers” generates bivalence through use of an asymmetrical decision mechanism. Many of these situations can be at least partially modeled with single options. Thus, Mitchell and Pulvino (2001) analyze the market exposure of merger arbitrageurs in terms of writing naked put options on the market index. Using a non-linear, local regression between a merger arbitrage return data and a broad equity market index, Lhabitant (2004, p. 208) arrives at something that looks remarkably like the payoff diagram for a short put position on the market index.

The intuition that this model captures is that in many cases a sharp downturn in equity prices will cause a proposed merger to collapse, a circumstance that was witnessed on several occasions in 2008, so that, in effect, merger arbitrageurs capture a modest premium from selling such options most of the time, at a cost of occasional large losses. It is this embedded option that accounts for the negative skewness of their returns. It also accounts for the surprising degree of correlation between merger arbitrage – which, if properly structured as a fully hedged trade, would seem to be a market neutral activity – and the broader equity market.

An example of a model that employs long positions in options is provided by arguably the first attempt at such analyses, in Merton (1981) and Henriksson and Merton (1981), which was mentioned above. What this example has in common with the option-based analysis of merger arbitrage is that the model indicates that return streams from various investment techniques are sensitive not only to the direction of price developments in the underlying, but to its volatility as well. An example of a model that employs a two-option structure is provided by Fung and Hsieh (2001), who recommend the use of a lookback “buy” straddle (a trade structure consisting of long positions in put options that exercise at the maximum price of the underlying over some period plus call options that exercise at the minimum price) to model trend-following investment techniques. In this case, sensitivity to volatility is made quite explicit, since directional exposure to the underlying is hedged away, and price movement rather than price direction is the sole source of returns on this option structure. A similar model using conventional rather than lookback options can be used as an analogy for return-generating, if not precisely “investment,” techniques such as market making, which are also sequentially long and short, although not generally trend following.

Sensitivity to volatility

The probability that the underlying security will reach an option’s strike price is clearly a crucial determinant of the option’s value, and the probability is a function of the volatility of the underlying over the time remaining until the expiry of the option. Algebraic manipulation of option-pricing formulae allows us to solve for the volatility implied by the option’s price, but given the influence of supply and demand on the pricing of traded options, what is obtained from this exercise is not purely the option’s embedded volatility forecast. Although it is intuitive that implied volatility should relate to the probability of an option’s exercise, in fact the quantity combines the separate influences of a probability estimate with the market maker’s markup.

Nevertheless, an option’s price is quite sensitive to the volatility of its underlying, and while it is not possible to isolate the implied forecast, it does not follow that the implied forecast is not fully reflected in the option’s price – only that an additional factor is as well. Volatility may be beneficial to an investment technique, in which case modeling generally involves long option positions exercisable into a volatile underlying, or detrimental, in which case modeling generally involves short positions. This is consistent with the view that a forecast of volatility is implicit in option pricing: long positions involve purchase of volatility and short positions the sale of it.

There has been considerable discussion in option trading circles about whether volatility is an exploitable asset. That it can be traded through the use of options structures is unquestionable – an option “buy” straddle, like the structure mentioned above, is a classic means of obtaining relatively pure exposure to the volatility of the underlying without exposure to its price direction. The apparent ability to purchase volatility directly, through use of VIX Index or similar instruments, is in fact only apparent: these indices are, at bottom, simply synthetic straddles. Volatility is epiphenomenal: it is always an emergent property of something else.

This does not disqualify volatility as an exploitable source of returns. Other epiphenomena such as illiquidity premia, and for that matter interest rates (which are derived quantities that John Maynard Keynes struggled mightily to explain), are familiar to investors, and there are numerous investment techniques that generate their returns from them. However, what distinguishes volatility is that, through derivative structuring, it can generate returns without accompanying exposure to the directional movements of the underlying. I am uncertain where the notion that volatility is an “asset class” comes from – the earliest reference I have uncovered is from 2004 – and I find the notion of an epiphenomenal asset peculiar, but volatility is certainly an isolable source of returns. Since it can produce returns on its own, it can also contribute, positively or negatively, to the returns of various investment techniques in which its influence is not isolated, and clearly it does.

There are quite a few investment techniques that depend on volatility for their returns, but cannot tolerate too much. For example, yield curve arbitrageurs rely on volatility to create the pricing discrepancies that they exploit, but many find it difficult to put their trades in place if volatility becomes excessive. Their activities can be modeled with short strangles, a derivative structure which is profitable within a range of volatilities, but if the range is exceeded, produces losses.

Ability to exercise

In the usual definition of an option as “a right, not an obligation […]” the right is possessed by the owner rather than the writer of the option: the writer of an option explicitly sells that right to its counterparty. Ownership of such a right is a real option, conferring a power to choose outcomes, while a seller of the right grants that option to its counterparty. In many of the models discussed above, the sale or purchase of the right is not explicit.

Since options have value, the purchaser of one must pay for it in some way and the seller of one must be compensated for it in some way. In the context of using options to model investment techniques, the transaction is rarely so obvious to observation. Purchasers generally pay for options in the form of their investment in decision tools or trading infrastructure. For example, a tactical allocator must develop the indicators that drive its investment choices, while a market maker must accumulate a staff of traders or develop software in their stead. These expenditures in effect buy real options for the managers who make them. For investment techniques that can be modeled using short positions in options, the counterparty to the “trade” can be regarded as that amorphous entity, “the market.” The premium received is the return on their investment activities and the short position represents the risk, which accompanies their approaches to return seeking. This suggests that the unleveraged returns received are comparatively low and most of the time fairly stable, which is why short option models find ready application to arbitrage and other “absolute return” techniques, as well as in the Bookstaber/Jacob analysis of corporate credits.

Where the analogy with financial options breaks down, however, is on the issue of pricing. The apparently pristine mathematics of option pricing models mask the fact that actual practice includes an unanalyzed element that I referred to earlier as an option’s markup, but this is a comparatively minor matter. The “premia” paid by some investment practitioners can be substantial and variable – consider the fleets of analysts that many asset management firms employ – while the “premia” received by others are conditional on their investment performance. The analogies between investment techniques and various option strategies must not be pushed too far.

Additional issues regarding modeling with options

In fact, if we pursue the analogy, we also discover that strike prices and the volatility relevant to the options’ pricing are also undefined in most of these models, the Henriksson/Merton model being the major exception. Since these models are offered as general observations about this or that class of investment techniques, this should probably not be surprising: Henriksson and Merton were analyzing a specific strategy whose practitioners are fairly consistent with each other, and this is hardly the case with many of the others discussed above. However, this should not obscure the point that in many of these models the specific characteristics of the options to which their practitioners are said to have exposure cannot be specified.

Thus, while excessive downside volatility certainly provides unfavorable conditions for merger arbitrage, how much is excessive? Even in the thick of the recent market drama, which scuttled a number of deals, some mergers managed to close – notably including the largest all-cash transaction ever, Inbev’s purchase of Anheuser-Busch, despite the considerable difficulties that financial turmoil placed in the way of its completion. For trading techniques that exploit rather than suffer volatility, the payoff diagrams for their option-like structures would seem to make it quite clear that the price of the “premia” they incur dictates the amount of volatility they require or can tolerate in order to earn their returns. However, this is not in fact the case: profitable levels of volatility are dictated by the trade a manager chooses to pursue rather than the investment it makes in the infrastructure needed to pursue it.

Models that ascribe short option positions to investment techniques can readily accommodate leverage – increasing the short position provides a satisfactory analogue to leverage, in terms of both the increase in potential return and the increase in risk. However, leverage cannot be so easily accommodated in models that involve long positions in options. The increase in “premia” paid in order to take on additional long option exposure does not adequately reflect the increased risk due to leverage. Where the “premium” represents the cost of a manager’s trading or decision infrastructure, it will probably remain more or less unchanged regardless of how much leverage the manager takes on. The effects of leverage are linear and symmetrical, which accounts for the inability of long options positions to model it, but short positions provide a model that can take account of leverage for those trades, such as arbitrages, that have inherently limited positive return potential.

Options frequently encounter difficulties when they are used to model-hedged directional investment techniques (as opposed to arbitrages). This may seem paradoxical, given that options are often used as hedges. Take for example, a market-neutral technique that hedges long positions in equities with short positions in the appropriate index derivatives. Assuming that the equities employed retain their correlation to the indices held short, then such a fund accepts pure specific risk: its returns are linear and it displays no optionality, apart from the likely skewness that the specific risks themselves exhibit. However, if the correlation changes, optionality asserts itself, potentially in a very dramatic way. Figure 2 shows that such changes can be quite frequent. For the entire period shown, the extent to which changes in the index could be said to explain changes in the price of Procter & Gamble was moderate, at 0.29, but it varied between negligible and very significant, and sometimes changed quite rapidly. As with models that employ short put positions as analogies for investment techniques, in this case the option is “exercised” by the market rather than held long in the fund and exercisable at its manager’s discretion. However, it is not clear until it is “exercised” what type of option it might be: whether the fund is short a put or a call depends on how the security’s correlation to the hedge changes. Options do not provide a satisfactory model for an investment technique such as this.

Notional leverage

One cause of the asymmetry of options’ returns is the leverage that is embedded in them. This is often referred to as notional leverage, although it is not so much notional as blindingly explicit in the case of long positions in options. For example, once a call option is in-the-money, its holder has a claim on an asset that is worth more than the sum of the premium paid to obtain that claim and the exercise price. The situation parallels that of a purchaser who borrows a portion of the asset’s purchase price: in both cases, the return on the investor’s capital employed is greater than the appreciation of the underlying asset. The analogy is not exact, however, since the return patterns of a call option that expires at or out of the money are different from the symmetric returns achieved by a leveraged purchaser. Since it is a distinct form of leverage it requires a distinguishing moniker, and “notional” is the one that it has received.

It is in the case of short positions in options that their embedded leverage may be more properly be regarded as notional. A 2005 purchaser of an AA-rated Lehman Brothers bond would have received such a small premium for the far out-of-the-money short put position on Lehman Brother’s equity that was implicit in the bond that it probably went unnoticed. Most such investors would in fact have regarded the bond as essentially fungible with any other financial services issuer’s AA-rated bond – which, after all, is a large part of the point of using credit ratings as portfolio construction tools. It is through failure to attend to such notional exposures that most of the damage resulting from accidents in the derivatives markets occur.

Since, in most cases, they can be modeled as long positions, the leverage embedded in real options is generally quite explicit. However, where information or ability to exercise real options is asymmetric, the leverage may be less obvious to the option’s holder. This gives rise to the distinction used in real estate circles between market value and investment value, and the similar notion of private market value in public equity markets. Thus, a skilled developer may perceive an investment value in a property that its present and less-skilled owner regards as fairly valued at market price, and obtain a notionally leveraged return by purchasing the property and exercising that option.

Degrees of optionality

It would seem logical that optionality would share with symmetry an “either/or,” bivalent character – so that an investment technique would either exhibit it or it not – but as with asymmetry, that there would be degrees of optionality. However, optionality does not reduce to just the asymmetry of the distribution of returns. Exercisability and whether the model calls for the option to be held long or short are bivalent (unless the model employs more than one option), while sensitivity to volatility may be either bivalent or linear. In light of this, it is difficult to discern what greater or lesser optionality might mean.

In the case of real options, it seems straightforward to regard greater optionality as the possession of more options. This would imply, for instance, that an asset allocation vehicle that is restricted to holding only equities or cash has fewer options than one that can also invest in bonds, commodities, etc. and it seems reasonable to regard the latter as having greater optionality. Strictly speaking, however, the constrained vehicle has an infinity of options, given a continuum between 0 and 100 percent exposure. The apparently greater number of options available to the less constrained vehicle is not a higher order infinity. While this may seem like quibbling, and it is certainly counter to commonsense, that is not infrequently the case with the mathematics of infinity. Both are identical in size to the infinite set of real numbers, which Georg Cantor denoted with “α” (Aleph) as opposed to the “smaller” infinite set of natural (counting) numbers, which he denoted with “α0.” Consequently, the variety of options available to a manager cannot be used to establish degrees of real optionality in any formal sense. As a practical matter, however, exposure comes in quanta of useable measurement. If we assume that these are units of 0.001 percent of the total portfolio, then the constrained allocator has 100,000 options and the less constrained one has multiples of that figure, depending on the number of asset categories available to it.

It is a peculiarity of real, in contrast to familiar financial options, that in most cases their exercise results in the creation of one or more new options. The research and trading infrastructure that constitute the “premia” paid by a firm that possesses such options are not consumed through use, so that each allocation decision opens up the possibility of subsequent reallocation. The extent to which this process results in stable or increasing numbers of options might also be regarded as a degree of optionality. This is perhaps best illustrated with private market real estate. Short of the decision to demolish its property, the owner of an investment in prime office space has comparatively few options: it may change its financing arrangements, it may seek to raise its lease income, it may make comparatively minor improvements to its property, or it may dispose of it. In contrast, the owner of raw land has options that are only limited by its financial resources and the locality’s flexibility on zoning. However, each “exercise” by the owner of raw land reduces its subsequent options: the decision to build a parking garage, for example, cancels the option of building a medical facility.

However, it is far more difficult to come to any sense of degrees of optionality in the case of investment techniques that are modeled with options held short, where the investor has “sold” the right to “exercise.” In these cases, the number of options is an irrelevance, since it is a Δ-adjusted function of the exposed portion of the portfolio. It might be tempting to think that the probability of exercise – how near or far the option is to being in-the-money – gives one investment vehicle greater optionality than another, but this cannot be the appropriate metric, if for no other reason than that these models generally assume that the options are far out-of-the-money at time of purchase. Given that most of them employ short put positions, their optionality consists in the possibility of extreme adverse consequences, which is ever present. Such investment techniques do not exhibit degrees of optionality: they are all vulnerable to whichever catastrophic occurrence the short put positions are intended to model. Instead, the degree to which the options are out-of-the-money is the measure of how remote that possibility is.

Optionality and fund replication

Replication of hedge funds’ alleged β has attracted considerable interest in the last several years. To the extent that replication vehicles fulfill their function, they will also replicate the optionality of the hedge funds they are intended to mimic. This should hold true regardless of the method used to create the replication. It is explicit in the case of replication strategies that employ trading algorithms to reproduce investment techniques that possess real options, such as trend following – the decision mechanisms that their algorithms express embody those options. It may be less obvious if multi-factor analysis is employed to replicate hedge fund return streams, but it must be present if these vehicles can properly be said to replicate anything at all.

Of greater interest, however, is the question whether replication adds optionality to such vehicles that is not present in hedge funds’ alleged β. That is, do replication vehicles contain additional, perhaps hidden exposures that are not present in the funds they endeavor partially to mimic? This would represent additional, unanalyzed risk, and in the nature of the case it is impossible to demonstrate conclusively that they do not. More to the point, is it likely that they do? This seems probable.

A purely passive approach to factor-based replication would require that the correlations and the standard deviations among the instruments used to craft the replica and the fund being replicated, as well as the correlations among those instruments themselves, remain stable. Since this is highly unlikely over any appreciable period of time, a program of rebalancing is essential to maintain the hedging relationships among the various instruments used. This in itself represents a conditionality that might well be modeled using long positions in real options, for all that the rebalancing program can be specified algorithmically and thus retain a certain passive character.

However, assuming that rebalancing is frequent – that the time separating the real options’ “exercise dates” is short – such procedures are unlikely to contribute any substantial risks that could not in principle be analyzed. These risks would come instead in the form of undetected short put positions and in particular from their notional leverage – for the obvious reason that what goes unrecognized will remain unanalyzed. The more complex the replica, in terms of its number of components, the greater the likelihood that this will occur. This is analogous to the multi-body problem familiar from classical mechanics – the apparent impossibility of specifying with complete precision the orbits of a closed system containing more than two bodies.

Although physics has made some strides toward a generalized solution of this problem, which results from the feedback loops introduced by gravitational interaction among bodies, the mathematics involved is daunting and the solutions are neither applicable in practice nor can they take full account of singularities, such as those resulting if two or more of the bodies collide. This problem has attracted the attention of some of the finest mathematical minds – including Newton, Euler, Lagrange, and Poincaré – for nearly 3 and Quarter centuries. The parallel econometric problem is far more intractable. The relationships among the components of a replica are far more complex than the simplicity of the inverse square law that specifies gravitation, and singularities, as witnessed by the non-normality of price series, are far from uncommon. Users of factor-based replication products would be wise to assume that they are exposed to unanticipated optionality.

John AbbinkHudson, Ohio, USA : JABBINK@roadrunner.com

References

Agarwal, V. and Naik, N.Y. (2004), “Risks and portfolio decisions involving hedge funds”, Review of Financial Studies, Vol. 17 No. 1, pp. 63–98

Bookstaber, R.M. and Jacob, D.P. (1986), “The composite hedge: controlling the credit risk of high yield bonds”, Financial Analysts Journal, Vol. 42 No. 2, pp. 25–36

Fridson, M.S. (1994), “Do high-yield bonds have an equity component?”, Financial Management, Vol. 23 No. 2, pp. 82–4

Fung, W. and Hsieh, D.A. (2001), “The risk in hedge fund strategies: theory and evidence from trend followers”, Review of Financial Studies, Vol. 14 No. 2, pp. 313–41

Henriksson, R.D. and Merton, R.C. (1981), “On market timing and investment performance II: statistical procedures for evaluating forecasting skills”, Journal of Business, Vol. 54 No. 4, pp. 513–33

Kocagil, A.E. (2004), “Optionality and daily dynamics of convenience yield behavior: an empirical analysis”, Journal of Financial Research, Vol. 27 No. 1, pp. 143–58

Lhabitant, F.-S. (2004), Hedge Funds: Quantitative Insights, Wiley, Chichester

Merton, R.C. (1981), “On market timing and investment performance I: an equilibrium theory of value for market forecasts”, Journal of Business, Vol. 54 No. 3, pp. 363–406

Mitchell, M. and Pulvino, T. (2001), “Characteristics of risk and return in risk arbitrage”, Journal of Finance, Vol. 56 No. 6, pp. 2135–75