Citation

Wilhelm, T. (2012), "The incorporation of sustainable features in commercial property valuation", Journal of Property Investment & Finance, Vol. 30 No. 4. https://doi.org/10.1108/jpif.2012.11230daa.002

Publisher

:Emerald Group Publishing Limited

Copyright © 2012, Emerald Group Publishing Limited

The incorporation of sustainable features in commercial property valuation

Article Type: Practice Briefing From: Journal of Property Investment & Finance, Volume 30, Issue 4

A review of theory and practice in the UK

Introduction

The valuation profession has a central role within the property market as they advise clients on sustainable property features and their effect on market value. Valuers are able to support the allowance of sustainability in the property world however they are hampered by a lack of data and knowledge. Consequently, comparative valuation methods are limited in reflecting benefits of sustainable property and valuers are not able to demonstrate the added value at this stage.

In the last 20 years the issue of sustainability and sustainable development has been an emerging topic, initiated by the publication of the Brundtland Commission report (WCED, 1987). The Stern Review on the Economics of Climate Change argued that the overall costs of the climate change would be equivalent to losing between 5 and 20 per cent or more of global gross domestic product (GDP) each year (Stern, 2006). This shows that the rising awareness of sustainability and the impact on the global environment is becoming more and more important for the overall economy. Buildings account for more than 40 per cent of the carbon emissions, 30 per cent of the solid waste generation and 20 per cent of water emissions as well as use more than 40 per cent of total energy (Sayce et al., 2010) while the commercial property sector accounts for approximately 17-18 per cent of the total carbon emissions from energy use in the UK (Dixon et al., 2009).

These figures are alarming and it is becoming clear that an increase in the level of sustainability in the commercial property stock is important in order to reduce the negative impact of the built environment on the Earth’s ecosystem (Myers, 2012). Therefore, sustainability has to be seen has an opportunity as it establishes a relationship between economy, environment and society (Boyd and Kimmet, 2005). These three principles are also known as “triple bottom line” and are widely adopted by both private and public sector as well as by organisations such as the Royal Institution of Chartered Surveyors (RICS) (Lorenz and Lützkendorf, 2005; RICS, 2009) (Figure 1).

Due to the fact that both insufficient market evidence and insufficient homogeneity of properties are major characteristics of the property market, valuers function as the assessors and advisors of market value (Baum and Crosby, 2008). Valuers have a central role within property markets as they are being consulted to proffer their opinion, judgement and assumptions in terms of sustainability features and the effect on market value (Myers, 2012). However, there is a lack of evidence to prove that sustainability has a positive effect on market value and therefore this fact is seen as a hurdle for investors to invest in “green” buildings (Sayce and Sundberg, 2009). If financial justification and viability of the required investment cannot be proven then there is a high likelihood that the advancement of sustainability in the commercial property sector will be inadequate (Myers, 2012). This is problematic since it might lead to a situation in which financial, human and natural resources are used inefficiently (Lorenz and Lützkendorf, 2011).

Purpose of research

This paper discusses the current research in sustainability in the property sector and sets this against a survey of UK based RICS accredited valuation professionals. This provides an insight of current valuation practice in the UK and helps to get a better understanding of key issues in terms of sustainability in property valuation. The main primary research objectives are:

- 1.

If valuation professionals account for sustainable property features in property valuation and how they do it?

- 2.

Whether sustainable issues in the property market are already considered as a market value increasing parameters?

- 3.

What is the importance of sustainability issues in property valuation?

- 4.

Is the guidance and support by professional bodies (e.g. RICS) seen as useful and sufficient regarding this topical issue?

The purpose of this research is to document whether the property industry is already aware of the increasing importance of sustainability in the property sector and if valuers are able to influence this situation by demonstrating the incorporation of sustainable property features within the valuation process. Therefore, the relationship between sustainable property features and market value is examined as well as the consideration of sustainability in property valuation.

The valuation process

According to Pagourtzi et al. (2003) a valid valuation must produce an accurate estimate of the property’s market price. Therefore, it essential that the valuation reflects market conditions and culture at the time of valuation as it represents underlying fundamentals of the market. In the case of property valuation, the valuer calculates the best estimate of the trading price of the building.

In this context, the following convention is adopted (French, 2004):

- •

Price is the actual observable exchange price in the open market.

- •

Market value is an estimation of the price that would be achieved if the property were to be sold in the market.

- •

Calculation of worth reflects the fundamental worth to an individual or group of individuals.

The formal definition of market value is contained in the valuation standards of the International Valuation Standards Council (IVSC) which states:

Market Value is the estimated amount for which a property should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion (IVSC, 2011).

Whilst price is the observable amount of money that is paid for a particular property, market value is the best estimation of the most likely price if the property were to be sold on the open market (Pagourtzi et al., 2003).

Worth is the maximum/minimum capital sum that an individual would pay/accept for the stream of benefits that he/she expects to be generated by the property (Lorenz, 2006). Again, defined by the IVSC (under the term investment value) as:

The value of property to a particular investor, or a class of investors, for identified investment objectives. This subjective concept relates specific property to a specific investor, group of investors, or entity with identifiable investment objectives and/or criteria (IVSC, 2011).

The distinction between market value and worth will be revisited later in the paper.

Property valuation has a central role within the property sector because the price of property is not discernible until the property is sold. Therefore, property valuation is one of the major sources of information within the investment decision-making (Lorenz, 2006). The function of the RICS is essential, as it is the professional body which sets the standards which members must adopt (French, 2005). In 2007, the RICS, the Appraisal Institute (AI) and others promoted the topic of sustainability within the property sector by signing the Vancouver Valuation Accord (2007).

It is worth mentioning that there is no universally agreed definition of sustainable property. However, an emerging consensus can be observed since the property market is becoming more aware of this issue and new metrics and regulations are developed and introduced (RICS, 2009). The best-known and most widely accepted definition is that produced by the Brundtland Commission report:

Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs (WCED, 1987).

Even though the awareness of sustainability issues in the property sector is rising, there is no clear understanding and implication of sustainable property features within the investment decision (Sayce and Sundberg, 2009). Although sustainability principles may be included in the policies of property owners and occupiers (Dixon et al., 2009), it is still difficult to translate them to their property decisions. This is because not all characteristics in terms of sustainability can be easily demonstrated or translated into market value (RICS, 2009).

The role of the valuation profession

Every member of the RICS employed as a valuation professional must carry out his valuations in accordance with the RICS Professional Valuation Standards (RICS, 2012), also known as the “Red Book” (French, 2005). Therefore, it is obvious that the RICS, as a professional body within the property sector, has a major role and responsibility towards the consideration of sustainable issues within the valuation process. In 2009, the RICS published its first valuation information paper which explicitly deals with sustainability in valuation (RICS, 2009).

If the market does not differentiate between a sustainable building and a conventional counterpart then there will be no difference in market value (RICS, 2009). In order to account for a factor (e.g. sustainability) within valuation process, it is necessary that evidence for demand exists for this factor and that investors and/or occupiers are willing to pay a premium (Pleydell-Bouverie, 2006). Nevertheless, it has been also argued before, that sustainable property characteristics will not have any effect upon the rental or transaction price agreement of a building (French, 2008; Parnell and Sayce, 1999).

The role of the valuer within the property industry is essential, as the valuer must reflect the value of the building by assessing the property specific present and future risks (Reed, 2008). Only if an accurate estimation of market price is given, the valuation method can be considered as valid (French, 2004). In addition, valuations are necessary since there is both insufficient market evidence and insufficient homogeneity of properties, so that consequently market participants are not able to fix prices (Baum and Crosby, 2008).

Since market valuation needs to estimate the most likely sale price, the valuer has to incorporate sustainable property features only to the extent to which these issues affect the competitive position of property assets. It is the valuer’s role to reflect these benefits otherwise the valuation reports will lead to misleading price estimates (Lorenz, 2006).

Implementation into valuation practice

Valuers need to recognise that buildings, built according to certain “green” standards, may be more valuable than those that do not show the use of such standards (Guidry, 2004). It was argued that if market participants are in favour of sustainable properties then this has to be reflected in market value (Lorenz and Lützkendorf, 2008). The authors investigated the most significant parameters for an investor when making an investment decision: return and risk. They can show that sustainable property features positively influence both parameters and that these benefits can be reflected in property valuation. Sayce et al. (2004) developed a working model which allows the incorporation of sustainable property features into calculations of worth. The model has been simplified and reduced to the four key variables:

- 1.

rental growth;

- 2.

depreciation;

- 3.

risk premium; and

- 4.

cash flow.

These variables are influenced by specific sustainability criteria. The selection, classification and weighting of these criteria have been developed with the help of professionals in the property sector, investors and occupiers. As the model is dealing with the calculation of worth and not with the calculation of market value, it is not directly relevant to market valuations but, over time, one would expect that specifications that add to the worth of a building will be reflected in increased values over time. The purpose of the research is to see if this can be identified in practice.

The survey

The survey focused on RICS accredited valuation professionals working with property surveying firms in the UK. The survey was to a small targeted sample (20 responses) and thus the results are indicative rather than statistically significant. Likewise, the survey was undertaken in June/July 2011 and thus is a cross-sectional approach; it offers only a snapshot of current valuation practice in the UK.

Table I. Top chartered surveyors by UK turnover

The heads of valuation in several well-established surveying firms in the UK were contacted by e-mail with the request to forward the attached questionnaire to all valuation individuals at the subject firm (Table I). Furthermore, the author used the RICS web site in order to get the contact details of all registered surveying firms which offer commercial valuations in the UK (RICS, 2012). All responses were anonymous and confidential at the non aggregate level.

Profile of respondents

There were 20 respondents representing all degrees of seniority from director/partner to valuation surveyor. Figure 2 provides an overview of the working experience of the respondents as RICS accredited members. It shows that more than 65 per cent of the respondents had working experience of more than 16 years, which supports the reliability of the completed questionnaires. The average post qualification experience was 24 years, which is also quite high and underlines the previous argument.

Abbreviations: Question 1. How would you best describe your level of awareness of sustainability in property valuation?

All respondents regarded their own awareness of sustainability in property valuation at least as “moderate”, while 45 per cent have a good understanding.

Question 2. How would you describe your awareness of the incorporation of sustainability in property valuation relative to your peers? What makes you feel this way?

In total, 11 respondents said that they have the same awareness of the incorporation of sustainability in property valuation relative to their peers. Seven indicated “higher” and only one indicated “very high”.

Question 3. Do you know the Vancouver Valuation Accord (VVA) and if yes, are you aware of the importance and consequences for the valuation profession?

In total, 13 respondents did not know the VVA and only six knew the VVA and were aware of the importance and consequences. One respondent knew it but was not aware of the importance and implications for his/her profession.

Question 4. Do you currently account for sustainable issues in property valuation?

Only 55 per cent of the respondents currently account for sustainability in property valuation. Surprisingly, although all respondents indicated their level of awareness of sustainability in property valuation at least as moderate, more than 45 per cent do not account for it.

Question 5. If you ticked yes (previous question), could you please describe how you account for sustainable issues in property valuation?

From the 11 valuers who stated that they account for sustainability issues, six do this by direct adjustment of key variables only. One respondent accounts by direct adjustment and lump sum adjustment and one respondent both and with the help of the calculation of a sustainability-correction factor. Three respondents stated that they account for sustainability issues by other methods.

Question 6. How long have you accounted for sustainable property features in property valuation?

Most of the respondents have accounted for sustainability in property valuation for less than five years. This indicates that sustainability has been a rising issue in the last decade in the property sector.

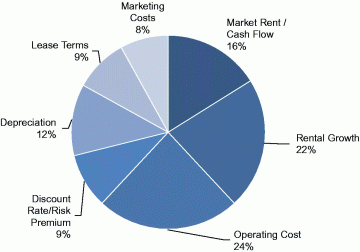

Question 7. What are the key variables in market valuation in order to reflect sustainability?

Figure 3 shows that the most important key variables are “operating costs”, “rental growth” and “market rent”. It indicates also that the “discount rate/risk premium” does not play a major role when reflecting sustainable property features in valuation practice. The same also applies for “depreciation”, “lease terms” and “marketing costs”. It was argued by one respondent that the most important factor in future will be imposed tax charges in order to reflect the sustainability rating which would have significant impact on all of the points highlighted above.

Question 8. In your opinion, is sustainability a major factor for investors when investing in commercial property?

More than 55 per cent of the respondents. Two respondents were not sure. It has to be acknowledged that two valuers commented that this also depends on the public nature of the investor and on the subject property.

Question 9. Which of the following benefits do you consider as most important for investors when investing in sustainable property?

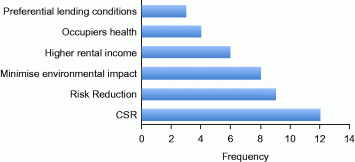

The most important benefit for investors from the view of a valuer is corporate social responsibility (CSR). This underlines the fact that investing in sustainable property is part of the companies’ CSR strategies as well as to increase the shareholder value. Investors are not only interested in higher rental income and risk reduction but also see the importance of CSR and the related positive effect of communication (Figure 4). The same applies to the benefit of minimising environmental impact trough the life cycle of the building.

Question 10. Do you agree that because of a lack of “sustainable” comparables valuers are not able to quantify benefits?

About 70 per cent of the respondents stated that they are not able to quantify benefits occurring due to sustainable property features because of a lack of sustainable comparables. It was also stated by one of the respondents who disagreed, that “[…] such comparables may be helpful, of more relevance is understanding the impact of obsolescence/depreciation on less sustainable stock and the consequent impact on value”.

Question 11. Do you agree that valuers should have an informational duty to inform their clients on sustainable benefits as they might influence the value stability and value development of the subject building?

Again the majority see it as their duty to inform their clients about sustainable benefits and therefore to bring forward this issue as well as the allowance of sustainability in the property sector (Figure 5).

Question 12. Do you agree that valuation is major source of information for investors within their investment decision-making?

In total, 16 respondents “agreed” or “absolutely agreed” that valuation is a major source for investors. Therefore, it could be argued that valuation has a central role in the property sector as investors base their decisions on valuations. One respondent did not answer this question.

Question 13. How do you inform yourself about current guidance⁄recommendation in terms of sustainability in property valuation?

Even though the RICS has a strong standing in the UK, it is not the only source of information for valuers. Seminars, information provided by the company, conferences and lectures as well as EGI are also key sources (Figure 6).

Question 14. Do you think that you receive good guidance in terms of sustainability in property valuation provided by organisations such as the RICS?

The following results are consistent with the literature review since both academics and professionals do not feel sufficiently guided and informed by the RICS in respect of the topical issue. This is a clear sign that the RICS and other professional bodies need to react to this deficit.

Conclusion

The survey has highlighted that sustainable issues are only reflected in value if the market considers that sustainability is of greater worth to them. This occurs because occupiers and investors show little or no demand for “green” buildings and that the valuation profession is challenged by a lack of comparables. As long as the “demand” side does not integrate SRI into their investment policy, sustainability is not having any value increasing effect on the market value of “green” buildings.

Valuers only mirror the market and if the market demands sustainable property features then this will be reflected in market value. On the other hand, as property professionals, it can be argued that valuers have a central role in the property market and are therefore perfectly placed to bring forward this issue. They do have the market experience and the knowledge to support SRI indirectly by showing potential benefits for both investors and occupiers.

It has been demonstrated that the “demand” side of the property market needs to raise their awareness of sustainable issues in the property sector. The survey has shown that even though the majority of the respondents felt responsible it was also argued that valuers only mirror the market so that the initial input has to be given by investors and occupiers. However, it has to be questioned how the “demand” side shall be informed about potential benefits of sustainable building if not by the valuation profession.

It is a point of fact that valuers already see it as their duty to contribute towards the allowance of sustainability in the property sector. Valuers function as the assessors of market value and are being consulted for their professional opinion. Therefore, it is recommended that valuers provide recommendations and informational services towards sustainable aspects in their valuation reports. This may include a documentation of risks, a separate chapter on sustainability and a sensitivity analysis. This will concentrate the attention of investors and occupiers on the benefits and on the decreased risk exposure of sustainable buildings. In addition it will improve the understanding of the valuation process and finally result in an improved data basis of the decision makers.

Tobias Wilhelm

References

Baum, A. and Crosby, N. (2008), Property Investment Appraisal, 3rd ed., Blackwell, Oxford

Boyd, T. and Kimmet, P. (2005), “The triple bottom approach to property performance evaluation”, Proceedings of the 11th Annual Pacific Rim Real Estate Society (PRRES) Conference, Melbourne, Australia

Dixon, T., Ennis-Reynolds, G., Roberts, C. and Sims, S. (2009), Demand for Sustainable Offices in the UK – Summary Report, IPF Research Programme 2006-2009, March

Estates Gazette Interactive (EGI) (2010), “Heavy weather – the 2010 EG top agents survey shows the industry in its second year of recession”, Estates Gazette, 11 September

French, N. (2004), “The valuation of specialised property – a review of valuation methods”, Journal of Property Investment & Finance, Vol. 22 No. 6, pp. 533–41

French, N. (2005), “The little red book”, Estates Gazette, Vol. 15, October

French, N. (2008), “The valuation of sustainability and green leases”, The Conveyancer, Vol. 72 No. 6, pp. 517–24

Guidry, K. (2004), “How green is your building? An appraiser’s guide to sustainable design”, The Appraisal Journal, Vol. 72 No. 1, pp. 57–68

IVSC (2011), International Valuation Standards 2011, 8th ed., International Valuation Standards Council, London

Lorenz, D. (2006), “The application of sustainable development principles to the theory and practice of property valuation”, dissertation, Karlsruher Schriften zur Bau-, Wohnungs- und Immobilienwirtschaft, Band 1, Vol. 1, Universitätsverlag Karlsruhe, Karlsruhe

Lorenz, D. and Lützkendorf, T. (2005), “Sustainable property investment: valuing sustainable buildings through property performance assessment”, Building Research & Information, Vol. 33 No. 3, pp. 212–34

Lorenz, D. and Lützkendorf, T. (2008), “Sustainability in property valuation: theory and practice”, Journal of Property Investment & Finance, Vol. 26 No. 6, pp. 482–521

Lorenz, D. and Lützkendorf, T. (2011), “Sustainability and property valuation – an international review and systematisation of existing approaches”, Journal of Property Investment & Finance, Vol. 29 No. 6

Myers, G. (2012), “The value of sustainability in real estate: a review from a valuation perspective”, Journal of Property Investment & Finance, Vol. 30 No. 2

Pagourtzi, E., Assimakopoulus, V., Hatzichristos, T. and French, N. (2003), “Real estate appraisal: a review of valuation methods”, Journal of Property Investment & Finance, Vol. 21 No. 4, pp. 383–401

Parnell, P. and Sayce, S. (1999), Attitudes Towards Financial Incentives for Green Buildings, Kingston University School of Surveying and Drivers Jonas Property Consultants, London

Pleydell-Bouverie, N. (2006), “Will EPBD certification significantly improve the energy efficiency of the Central London office stock? Assessing the implementation requirements for the success of energy certification”, MSc dissertation, Oxford Brookes University, Oxford, August

RICS (2009), Valuation Paper 13 – Sustainability and Commercial Property Valuation, Royal Institution of Chartered Surveyors, London

RICS (2012), RICS Professional Valuation Standards, 8th ed., Royal Institution of Chartered Surveyors, London

Reed, R. (2008), “Encouraging the uptake of sustainable buildings and the critical role of the property valuer”, SB 2008: Proceedings of the World Sustainable Building Conference, SB08, Melbourne, pp. 272–83

Sayce, S. and Sundberg, A. (2009), “Sustainable property: a premium product?”, Proceedings of the European Real Estate Society Conference, KTH University, Stockholm, 24-27 June

Sayce, S., Ellison, L. and Smith, J. (2004), “Incorporating sustainability in commercial property appraisal: evidence from the UK”, Australian Property Journal, August, pp. 226–33

Sayce, S., Sundberg, A. and Clements, B. (2010), Is Sustainability Reflected in Commercial Property Prices: An Analysis of the Evidence Base, RICS Research Report, January

Stern, N. (2006), Stern Review on the Economics of Climate Change, Cambridge University Press, Cambridge

Vancouver Valuation Accord (2007)

WCED (1987), Our Common Future: The Report of the Brundtland Commission, World Commission on Environment and Development, New York, NY

Further Reading

Berman, A. (2001), “Green buildings: sustainable profits from sustainable development”, unpublished report, Tilden Consulting, cited in Robinson, J. (2005), “Property valuation and analysis applied to environmentally sustainable development”, paper presented at PRRES Eleventh Annual Conference, Melbourne, Australia, The University of Melbourne, Melbourne

Ellison, L. and Sayce, S. (2006), “Assessing sustainability in the existing commercial property stock – establishing sustainability criteria relevant for the commercial property investment sector”, Property Management, Vol. 25 No. 3, pp. 287–304

Jones Lang LaSalle (2008), Transparency Index 2008, Jones Lang LaSalle, London

Kimmet, P. (2006), “Theoretical foundations for integrating sustainability in property investment appraisal”, Proceedings of the Pacific Rim Real Estate Society (PRRES) Conference, Auckland, New Zealand

Lorenz, D., Truck, S. and Lützkendorf, T. (2006), “Exploring the relationship between the sustainability of construction and market value”, Property Management, Vol. 25 No. 2, pp. 119–49

Matthiesen, L. and Morris, P. (2004), Costing Green – A Comprehensive Cost Database and Budgeting Methodology, Davis Langdon Adamson, San Francisco, CA

Phillips, D.C. and Burbules, N.C. (2000), Postpositivism and Educational Research, Rowman & Littlefield, Lanham, NY

RICS (2005), Green Value – Green Buildings, Growing Assets, Royal Institution of Chartered Surveyors, London

St Lawrence, S. (2004), “Review of the UK corporate real estate market with regard to availability of environmentally and socially responsible office buildings”, Journal of Corporate Real Estate, Vol. 6 No. 2, pp. 149–61