Citation

Curwen, P. (2004), "Is bankruptcy the end or the beginning?", info, Vol. 6 No. 2. https://doi.org/10.1108/info.2004.27206bab.001

Publisher

:Emerald Group Publishing Limited

Copyright © 2004, Emerald Group Publishing Limited

Is bankruptcy the end or the beginning?

A regular column on the information industries

Is bankruptcy the end or the beginning?

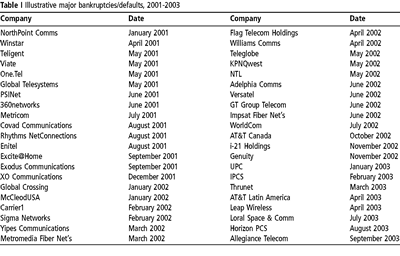

There have been an awful lot of bankruptcies in the technology, media and telecommunications (TMT) sector since the beginning of the new millennium. As a glance at the share price history of any TMT company reveals, share prices in the sector almost universally first rocketed then plunged within a two-year period. Since the upwards movement tended to reflect vast expenditure on building for a glorious future, it is hardly surprising that the downwards movement resulted in an inability to secure additional funds for investment and a severe absence of cash flow, leading to bankruptcy, administration and/or debt-for-equity swaps. Table I shows major bankruptcies/defaults 2001-2003.

It should be borne in mind that the list in Table I lays no claims to being comprehensive and that, in certain cases, restructuring has taken place outside the bankruptcy courts. For example, Qwest Communications International swapped $5.2 billion of debt for $3.3 billion of more senior, higher-yielding debt in December 2002, in order to stave off bankruptcy. Such behaviour is not uncommon in the USA where arrangements are also often made prior to declaring bankruptcy so as to expedite the process of emerging as quickly as possible with a cleaned-up balance sheet.

Most of the companies cited in Table I are American. One obvious reason is the sheer number of TMT companies in the USA compared to Europe, while another is the fact that European incumbents have been protected from bankruptcy by their sheer size and, sometimes, state ownership, with most new entrants being too small to register in the table where the liabilities often ran into the billions of dollars. However, the main reason is that bankruptcy is treated somewhat more leniently in the USA compared to, say, Europe. Under Chapter 7 of the US Bankruptcy Code, the assets of the debtor are liquidated and the proceeds are distributed to creditors. This conventional approach to bankruptcy, used widely in Europe, can be contrasted with the Chapter 11 procedure, unique to the USA, which permits the debtor to continue operating its business under protection from its creditors while developing a plan to enable it to trade profitably in the future. Not surprisingly, Chapter 11 cases predominate[1].

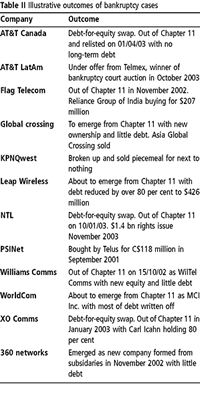

The underlying argument for Chapter 11 is that there are few, if any winners when bankrupt companies end up in liquidation. Surely, it is argued, it is better to salvage those parts of a bankrupt company that either already are, or potentially could be, profitable. Hence, the process of salvaging the potentially profitable parts of most of the companies in Table I was set under way as part of the Chapter 11 process. For example, WorldCom bought the assets of Rhythms out of bankruptcy, as did AT&T in the case of NorthPoint. AT&T followed up with a $307 million offer for Excite@Home in which it previously had a minority economic but majority voting interest, although it subsequently withdrew. However, there is a downside to fire sales of bankrupt assets (which still require that potential buyers retain a sufficiently high credit rating and sufficient cash to be active participants). In essence, the ability of operators to emerge from Chapter 11 proceedings with debts largely written-off – often by virtue of a debt-for-equity swap which leaves the former bondholders with all or almost all of the restructured company’s shares while its former owners emerge with little or nothing – inevitably puts further pressure upon former competitors which remain saddled with their own debts.

This can be illustrated in the case of WorldCom, which filed for Chapter 11 on 21 July 2002. This was the biggest bankruptcy in US history, involving $41 billion in liabilities, and was triggered by revelations of accounting “irregularities” that eventually amounted to $11 billion. Not surprisingly, this complicated the process of restructuring the company, as did in-fighting among the multitude of creditors, but it was anticipated that WorldCom would emerge in its new guise as MCI Inc. with no more than $4 billion of debt and cash-in-hand of $1 billion. Such an outcome not only offended competitors such as AT&T but generated widespread moral outrage among commentators, but it was argued that the vast majority of WorldCom employees had worked hard and kept within the law while often losing their pension rights held in WorldCom shares, so it was inappropriate to cause any more suffering than absolutely necessary.

Equally, Global Crossing, a company once worth $50 billion that had bid (unsuccessfully) for both US West and Equant but succumbed to debts of $25 billion, going into Chapter 11 in January 2002, nevertheless managed to sign deals worth nearly $1 billion with 2,000 new customers in 2002, followed by a further 2,220 new contracts worth $675 in the first half of 2003. Now 61 per cent owned by Singapore Technologies Telemedia (which paid a mere $250 million for the stake), with the rest held by former creditors, it openly admits that its financial position is sufficiently strong so as potentially to inflict severe damage upon its competitors via aggressive pricing should it so wish.

A further downside of bankruptcies which can occur, irrespective of whether the rump of a bankrupt company lives on, is that it inevitably leads to the dumping of relatively modern equipment onto the market at knock-down prices. This, in turn, causes inventory problems for companies seeking to sell the same or similar equipment at book prices. These factors explain, to a considerable extent, the timing of the recent cyclical pattern in the TMT sector. As shown in Table I, the big surge in bankruptcies occurred between mid-2001 and mid-2002. However, despite the apparent clear-out of uncompetitve companies, the fact that so many re-emerged with much less debt post-Chapter 11, as shown in Table II, combined with the need to dispose of or scrap unsold inventories, has meant that the first real signs of improvement in the economic wellbeing of the TMT sector have only emerged towards the end of 2003.

In recent times, it has become commonplace for so-called “vulture funds” to move heavily into the TMT sector. These funds specialise in the acquisition of bonds trading at substantial discounts to their face value in the hope that they will profit if there is a subsequent debt-for-equity swap, while taking the risk that even the bondholders will be wiped out via a liquidation. Operators anxious to make cheap acquisitions and gain control via the back door – c.f. Liberty Media in relation to various cable companies – also tend to favour this approach. In capitalism, it is said, the winner takes all, but there can be no doubt that many companies are emerging from Chapter 11 as potential winners when they should perhaps have gone into Chapter 7 as permanent losers to protect the (relatively) innocent survivors of the TMT meltdown. However, despite this there are many advocates pressing for the introduction of a form of Chapter 11 proceedings into Europe.

See www.1.worldcom.com/infodesk/chapter11

Peter CurwenVisiting Professor of Telecommunications at the Strathclyde Business School, Glasgow, UK.E-mail: pjcurwen@hotmail.com