Prelims

International Perspectives on Crowdfunding

ISBN: 978-1-78560-315-0, eISBN: 978-1-78560-314-3

Publication date: 20 July 2016

Citation

(2016), "Prelims", Méric, J., Maque, I. and Brabet, J. (Ed.) International Perspectives on Crowdfunding, Emerald Group Publishing Limited, Leeds, pp. i-xxxvi. https://doi.org/10.1108/978-1-78560-315-020151020

Publisher

:Emerald Group Publishing Limited

Copyright © 2016 Emerald Group Publishing Limited

Prelims

Half Title Page

International Perspectives on Crowdfunding

Positive, Normative and Critical Theory

Title Page

International Perspectives on Crowdfunding

Positive, Normative and Critical Theory

Edited by

Jérôme Méric

Université de Poitiers, France

Isabelle Maque

Université de Poitiers, France

Julienne Brabet

Université Paris-Est Créteil, France

United Kingdom – North America – Japan – India – Malaysia – China

Copyright Page

Emerald Group Publishing Limited

Howard House, Wagon Lane, Bingley BD16 1WA, UK

First edition 2016

Copyright © 2016 Emerald Group Publishing Limited

Reprints and permissions service

Contact: permissions@emeraldinsight.com

No part of this book may be reproduced, stored in a retrieval system, transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without either the prior written permission of the publisher or a licence permitting restricted copying issued in the UK by The Copyright Licensing Agency and in the USA by The Copyright Clearance Center. Any opinions expressed in the chapters are those of the authors. Whilst Emerald makes every effort to ensure the quality and accuracy of its content, Emerald makes no representation implied or otherwise, as to the chapters’ suitability and application and disclaims any warranties, express or implied, to their use.

British Library Cataloguing in Publication Data

A catalogue record for this book is available from the British Library

ISBN: 978-1-78560-315-0 (print)

ISBN: 978-1-78560-314-3 (online)

List of Contributors

| Bernardo Balboni | University of Trieste, Italy |

| Paul Belleflamme | Université Catholique de Louvain, Belgium |

| Adam J. Bock | Edgewood College Business School, Madison, WI, USA |

| Karima Bouaiss | University of Poitiers, France |

| Julienne Brabet | University of Paris Est Créteil, France |

| Denis Frydrych | University of Edinburgh Business School, Edinburgh, UK |

| Liz Gerber | Northwestern University, Evanston, IL, USA |

| Julie Hui | Northwestern University, IL, USA |

| Rémi Jardat | ISTEC, Paris and CNAM/Lirsa, Paris, France |

| Franck Juredieu | University of Tours, France |

| Tony Kinder | University of Edinburgh Business School, Edinburgh, UK |

| Ulpiana Kocollari | University of Modena and Reggio Emilia, Italy |

| Thomas Lambert | Erasmus University, Netherlands |

| Isabelle Maque | University of Poitiers, France |

| Sébastien Mayoux | University of Poitiers, France |

| Jérôme Méric | University of Poitiers, France |

| Sophie Nivoix | University of Poitiers, France |

| Gwenaëlle Oruezabala | University of Poitiers, France |

| Fatima Zahra Ouchrif | University of Poitiers, France |

| Ivana Pais | Catholic University of the Sacred Heart of Milan, Italy |

| Yvon Pesqueux | CNAM-LIRSA, France |

| Simon G. Peter | Institut Supérieur de Technologie de Libreville, Gabon |

| Jose Luis Retolaza | Deusto Business School, Bilbao, Spain |

| Leire San-Jose | University of the Basque Country, Bilbao, Spain; University of Huddersfield, Huddersfield, UK |

| Ritu Srivastava | BIMTECH, Greater Noida, India |

| Abbey Stemler | Indiana University, IN, USA |

| Jorge Renato Verschoore | Unisinos University, Brazil |

| Rovian Dill Zuquetto | Unisinos University, Brazil |

Foreword

The delay in U.S. equity crowdfunding legislation notwithstanding, crowdfunding has matured rapidly from what was effectively considered an online form of begging into a legitimate form of small business financing in under a decade. The industry continues to defy analysts with sustained exponential growth: equity crowdfunding in Europe grew by 116% between 2012 and 2014, while the reward-based variant grew by 127%. 1 Of course, this industry does not exist in isolation. The growing relevance of crowdfunding is tied to a wider trend toward empowerment in the digital age. Three key developments in particular come to mind, all of which have both been highlighted and reinforced by crowdfunding. Firstly, there’s a growing tendency to trust our peers, the “crowd,” over institutions. Younger generations in particular are more open to doing business with and being influenced by peers, friends and like-minded people than the institutions that have traditionally dominated our worldviews and lifestyles. The meteoric rise of the peer-to-peer marketplace is emblematic of this development. The financial services industry has proved more resilient to this democratization than most, but is now firmly under its disruptive influence. New technologies are cutting out the middlemen when it comes to all kinds of financial transactions, establishing direct funding channels between people. In simple terms, people with money and people in need of money are being connected more efficiently than ever before. We’re investing in each other on a massive scale. This disintermediation of banks by new, peer-to-peer, technology-led solutions has the potential to shake finance to its very core – and crowdfunding is leading the way.

Secondly, the growth of the sharing economy – crowdfunding included – has meant there’s truly never been a better time to be an entrepreneur. Those of us with entrepreneurial inclinations can crowdsource ideas, crowd-create products, crowdfund their ventures and market globally. We can collaborate with people anywhere in the world. European innovation hubs and incubators are filled with these young, budding crowdpreneurs who, after bootstrapping their business idea to pre-financing stage, get off the ground using the crowd. Oculus is the most famous example, Facebook buying the virtual reality start-up for a cool $2 billion just two years after its crowdfunding campaign. Crowdfunding is uniquely suited to innovative ventures.

Of course, one can extrapolate this trend to a wider social context. At their core, crowd-related practices such as crowdsourcing, online petitions and online donating are about bringing people together to achieve a common goal. The collective has never had so much power. The wisdom of crowds ensures that ideas deserving of financial or labor resources get it. At least, in theory. On a more fundamental level, if the industrial revolution was about consumption, the digital age is all about creation. Manufacturing, once little more than the output of things, is today increasingly based around people-powered processes and products that help us create and grow things collaboratively. The emphasis is on the process of creation itself. We’re seeing people take back control of the means of production. This new production model now has an established method of payment: crowdfunding.

The last but by no means least influential development linked to crowdfunding is democratization. In short, crowdfunding (in particular equity crowdfunding) promises to level the financial playing field by making high-level, top-of-market services more accessible to all kinds of customers, not just institutional clients and high-net-worth individuals. The quality of investment opportunities featured across European equity crowdfunding platforms were once available only to the financial elite, and came with a heavy price tag. Now, online funding platforms are enabling non-accredited investors (read: anyone) to purchase shares in high-growth start-ups and small businesses. Of course, these types of investments come with significant risk, but the point is that these platforms are opening up potentially lucrative investment opportunities to the general public that previously would have gone to banks, investment funds or private clubs, or not been funded at all. In this sense, crowdfunding is helping to raise the financial literacy of the general public while lowering the barriers of entry to the worlds of venture capital, angel investing, and stock trading. We may soon find that equity crowdfunding hits a glass ceiling in terms of its potential for democratizing the world of business financing; working alongside rather than replacing traditional forms of finance. However, there’s no doubt that the greater financial inclusivity brought about this still emerging phenomenon is a positive force.

Recent financial crises and stricter banking regulations have created a funding vacuum in the life cycle of small businesses. Grounded in a traditional, offline, vertical way of operating, banks today seem ill-equipped to keep up with funding demand in this digital age of entrepreneurship. Bootstrapped tech start-ups with flexible business models don’t have time to wait in line.

So, with the credit crisis fresh in our minds, we’re discovering a novel source of credit and trust: ourselves. The popular term to describe this movement is crowdfunding – a buzzword whose definition is conflated to mean all kinds of thing but that, at its core, is about financial inclusivity. It may never be perfect – as the original backers of Oculus Rift will tell you – but at least it’s more democratic. Crowdfunding platforms all over the world are paving the way for financial democracy.

The future will tell us whether crowdfunding will remain a niche in entrepreneurial finance or will fundamentally disrupt the way entrepreneurs raise funds in the future. However, measuring the societal contribution of crowdfunding should not be limited to its overall market size, just like the contribution of venture capital cannot be measured solely on its market size. Indeed, even in the United States the venture capital market looks very small compared to the banking sector; however, the contribution of venture capital to employment, innovation and economic growth is significant, mostly because venture capital funds invest in the early-stage of company development and in startups with high growth perspectives that others would find too risky to fund. This argument also holds for crowdfunding. The true impact of crowdfunding should be evaluated on its overall contribution to economic growth and its role as a catalyst in spurring entrepreneurial initiatives. In part, crowdfunding certainly offers funding opportunity for projects and startups that would otherwise not be funded by traditional players.

Also, crowdfunding can contribute to society and economic development in ways that other sources of funding (venture capital, business angel, banks) cannot. Most importantly, it may spur more entrepreneurial initiatives in the society. For instance, in equity crowdfunding, the crowd buys ownership in a startup that they will see grow “from inside,” since they will be able to follow the company’s development that helps them understand and grasp the challenges but also opportunities of starting own companies. Research has shown that entrepreneurship is generally not learnt in business schools but initiated by individuals who grew up in an entrepreneurial environment such as having parents or relatives who were entrepreneurs themselves. Crowdfunding has the potential to bridge this gap for many individuals in society who did not grow up in entrepreneurial environments. In other words, crowdfunding may create a “supply effect” by triggering entrepreneurship in the society, because the participating crowd may learn how to start firms as a result of investing in and following entrepreneurial companies. Such entrepreneurial spillovers are not achieved through venture capital or business angel funding, nor when individuals purchase shares in large, publicly listed companies.

That said, the recent developments made was accompanied by significant experimentation worldwide in the last year. Consolidation starts taking place, with some large and globally oriented platforms emerging and institutional investors taking part of the recent developments. At the same time, we observe a broad range to new developments and business models, as evidenced in different chapters of this book. The digitalization of communication through the Internet has made horizontal organizations more efficient and made it possible to communicate with a large crowd rather than rely on traditional intermediaries to obtain finance. At the same time, individuals that rely on crowdfunding are able to tap a crowd that is fundamentally different from traditional investors, seeking not only a compensation but also to collaborate, sponsor projects they like, helping others and see their sponsored project become reality. Research may help understand cost and benefits of these different developments. This book represents an ambitious step toward better understanding the functioning of crowdfunding, providing definitions, and offering insights into motivations of the crowd. It further sets an ambitious agenda for future research on the topic. The contributions made in this book are most welcome as they help understand where we are going. We therefore recommend this book to academic researchers, practitioners, and policy makers alike.

Armin Schwienbacher

Professor of Finance at Université Lille 2 and SKEMA Business School, France

Korstiaan Zandvliet

CEO of Symbid, The Netherlands

Introduction: International Perspectives on Crowdfunding

Introduction

It has taken just a few years for “crowd based” neologisms to become common parlance. They are used to depict new web-based practices to collect and gather resources (Castrataro, 2011). The term “crowdsourcing” was first used by Jeff Howe in 2006 in Wired (14.06). The trick consisted of replacing “out” with “crowd” as in “outsourcing.” Such a switch in words denotes a new management philosophy: ask an easily reachable “crowd” to raise funds, to bring up new ideas, or to appraise opinions. In the same context, the term “crowdfunding” was coined by Michael Sullivan in August 2006 when launching the “fundavlong” (videoblog incubator) project (Maguire, 2013).

Crowdfunding as an entrepreneurial phenomenon conveys a generalized recourse to the Crowd (Turner & Killian, 1957, Wallace, 1999) to replace traditional fund providers, such as banks, financial markets, venture capitalists, governments, etc. New technologies have facilitated the development of music and other media subscriptions, NGOs’ punctual operations, micro-financing of projects, etc. At a social and economic level, the progress of crowdpractices challenges the borders that have been settled for centuries between financial activities, industry, and individuals. In so doing, it calls for renewed management, regulatory, and governance practices.

Fundamentally, resource collection from the crowd is nothing new

Large scale charity fundraising and subscription systems seem to be as old as the hills. In fact, this shape of public sponsorship emerged in the eighteenth century. In 1884, a large subscription was organized to finance the pedestal of the Statue of Liberty. Jonathan Swift promoted a first shape of micro-credit, the Irish Loan Funds, in the 1700s. At the time, the press played a major role in gathering a crowd around those projects and facilitating a shift from individual sponsorship toward larger scale collective programs.

The novelty of what we could call “crowdpractices” lies in the opportunities afforded by the Internet, and thus in a new momentum for a proven pattern

The Internet holds the power to mobilize millions of users around affinities, interests, and issues focusing on social, artistic, entrepreneurial projects. Platforms are set up to organize fundraising by more or less specialized suppliers. Zopa, Kickstarter, or Ulule have become major actors in project financing (start-ups, charity or cultural projects, innovations). Together with companies who are already specialized in this area, banks are becoming more and more interested in developing their own crowdfunding platforms, as complementary services to venture capital and traditional loans.

Information technology allows those seeking funding to reach a wider public than traditional media. It also offers the possibility to develop new forms of collaborative work, as suggested by the Wiki model, or to inspire online debates to define new trends (Brabham, 2013).

Beyond the fad phenomenon (Abrahamson, 1991), can crowdfunding become a model?

The success of crowdpractices (that is new crowd-related social practices such as crowdsourcing, crowdfunding, online petitions) is justified by the subsumed wisdom of crowds (Surowiecki, 2004). More basically, companies or individuals who turn to this pattern find an “almost free” financial or labor resource, where rewards are potentially compensated by public supplies (Hosaka, 2008). In return, contributors expect from participation some material compensation (if possible), but they are above all paid for their commitment with social contact, intellectual stimulation, or simply entertainment (Brabham, 2010). New practices emerge from these communities of interest (Schenk & Guittard, 2011). The popularity of crowdfunding, as far as financing start-up businesses is concerned, is also due to common interests between investors and entrepreneurs. Ease of access and rapidity are probably the main assets of these fundraising mechanisms. Entrepreneurs may also be able to turn their social capital (i.e., their contacts on social networks) into financial capital. Beyond platforms, social networks are important pathways to communicate on projects and to attract potential investors. Thus the key of crowdfunding campaigns is based on the tight link between the range, the autonomy and the participation of social networks, as well as on the ability to manage online communities to publicize the project as far and as wide as possible. Investors draw satisfaction from taking part in emerging projects. Their contribution can also be compensated with rewards or rights to vote (Belleflamme, Lambert, & Schwienbacher, 2014). When committing to a determined program, crowdfunders must know exactly what their funds have been used for. The relation between contributors and project holders changes deeply as compared to traditional financing patterns.

We do not know, at the present time, if turning to the crowd is a sustainable or a temporary social phenomenon

The ability to reach a wider audience to raise funds needed a specific name. The fact that the term of “crowd” has been preferred to any other designation, either technological (web-based-funding), economic (micro-funding), or social (pair-funding) is probably not accidental. The collective unconscious and discourse associate the crowd with positive significance. The crowd is wise (Surowiecki, 2004); it is generous (Gerber, Hui, & Kuo, 2012); it is the ideal expression of collective will (Lawton & Marom, 2013).

In a context of disintermediation in finance and public action, there is no surprise to see an inflation of “crowd based” labels. Nevertheless, if we take a closer look, the notion of the crowd is extremely ambiguous (Bouaiss, Maque, & Méric, 2015). The first theorists of the crowd saw it as a locus of potentially destructive impulsiveness (Le Bon, 2009) where individuals swap their consciousness for a collection of “freed” unconscious minds (Freud, 1981). The crowd is also able to surrender to anyone (person or system) who satisfies its aspirations (from basic needs to religious or philosophical beliefs) or anyone who traditionally dominates (La Boétie, 1975). Finally, the crowd happens to show extreme indifference to the fate of some individuals or minorities (Le Bon, 2009).

The use of technology to gather crowdfunders throws up many questions as well. To what extent is it possible to consider a “virtual crowd” a crowd? What happens if what we still call ‘the crowd’ does not reach the materiality of mass meetings (excepting the case of flashmobs which is not used in the crowdfunding practice)?

Research on crowdfunding is highly needed to address those questions. It is developing, but still at a very early stage.

Descriptive studies are multiplying, more or less justified recommendations are accumulating, but crowdfunding is still a fuzzy research subject for many scholars, because it induces many questions and criticisms of established management, legal and governance frameworks. The aim of this book is to set a corpus of significant research in order to consolidate and stabilize knowledge and reflexivity around this new social phenomenon.

As far as crowdfunding is concerned, the need for theory is three-fold, to address both scholars and practitioners:

A need for positive theory. Crowdpreneurs, crowdfunders and researchers are committed to understanding how crowdfunding projects are organized, how (and why) they may succeed or fail and how governments consider this new practice and try to regulate it.

A need for normative theory. Crowdpreneurs and crowdfunders may need templates and “recipes” to develop (or to assess and take part in) projects. But beyond this basic knowledge, they also need to know which models are more efficient and how to legitimate their actions.

A need for critical theory. To make crowdfunding more sustainable than a managerial fad, reflexivity must be developed on its social and economic impact. If regulation and practice have to be oriented in one specific direction which one should it be?

In the first part of this book (positive theory) factual questions on crowdfunding are addressed and (if possible) answered. How do crowdfunders operate? How can individual behaviors lead to such big effects? Why do the public take part in such operations? Under which regulatory constraints do platforms and crowdpreneurs operate?

Practitioners and researchers are interested in knowing how decisions to fund are made, what are the main motivations of crowdbankers, but also the reasons why entrepreneurs raise funds through online platforms. At a macro level, the variety of the uses of crowdfunding creates some questions on their potentialities: what can they do and what do they fail to achieve? Is there a relation between the success of crowdfunding operations and the diffusion of innovation? The role of regulatory frameworks may have a strong impact on these potentialities. This part is structured around the following questions:

- –

How do the actors behave on the market? A lot is already known about entrepreneurs and funders. What about the role of platforms? (Chapter 1).

- –

How do individual actions produce macro-phenomena on the crowdfunding market? (Chapter 2).

- –

Who are the crowdfunders, why and how do they take part to such projects? (Chapter 3).

- –

What are the factors that explain successes and failures of CF campaigns? (Chapter 4).

- –

How does this general knowledge on CF markets and actors’ behaviors should orient crowdfunding Law and regulation? (Chapter 5).

In the second part (normative theory), contextualized methods and patterns are proposed to run crowdfunding projects.

Questions multiply about the organization of platforms, the relationships needed with stakeholders and how they impact project outcomes, the modes of subscription, the potential rewards, the duration of projects and how crowdpreneurs can be coached. How should projects be planned? And how do crowdpreneurs develop crowdbanker loyalty?

This book addresses these questions in an international context, using experiences from Europe, Asia, Africa, North and Latin America. Indeed the chapters address the following “how to” questions:

- –

How to provide ventures with sufficient legitimacy? Is it enough to succeed? (Chapter 6).

- –

Are there alternative patterns of fundraising? What about crowdlending as a specific category of crowdfunding practices (including the question of what to do of cash surpluses if some are to be collected)? (Chapter 7).

- –

How to manage networks in crowdfunding projects? (Chapter 8).

- –

How to organize an emerging CF market for MSMEs in specific economic or cultural contexts? The case of India will be examined (Chapter 9).

- –

Is crowdfunding Shariah compliant? (Chapter 10).

The third part of this book (critical theory) aims to create some context to consider crowdfunding as a social phenomenon. To which extent is it new? What is its social and economic impact under macro and micro perspectives?

From the macro point of view, crowdpractices help new economic and social models emerge, where disintermediation seems to be a central idea. Have developed enough experience to say it is just a fad or is it a phenomenon that will leave tracks (fashion, see Abrahamson, 1991)? Is crowdfunding comparable to micro-finance, or something radically different? Is it a radical new leverage for entrepreneurs, be they social or not? How can and should regulators adapt to turn these impacts into socially profitable and sustainable ones? Critical theory of crowdfunding is probably the less structured but also the most open field for future research, including an assessment of practices after a significant period of experiencing. The main critical questions this book arouses can be phrased as follows:

- –

Which factors do explain the development of crowdfunding is society? What is its potential impact? Is it sustainable or momentary? (Chapter 11).

- –

How to prepare a deep economic and social change from the legal point of view? (Chapter 12).

- –

Do the terms of contracts between crowdfunding stakeholders have to be rethought, especially in psychological terms? (Chapter 13).

These research chapters are preceded by a short preliminary literature review. It is based on a bibliographical database which has been set up by the editors. It draws the main trends of academic production on crowdfunding, and shows how scattered the field is at the present time.

Jérôme Méric

Isabelle Maque

Julienne Brabet

Editors

A Cartography of the Academic Literature on Crowdfunding

This preliminary chapter provides an overview of the present phenomenon and research literature on crowdfunding. In such an emerging research field, it is an attempt to consolidate present academic knowledge on this topic and addresses the questions still to be dealt with by researchers in disciplines such as management, psychology, sociology and Law.

Crowdfunding: An Overview of the Phenomenon

In the past five years, the development of crowdfunding has led to the emergence of hundreds of ‘crowdfunding platforms’. These platforms act as an intermediary, facilitating the transactions between the crowd of potential donors or investors and the project initiators.

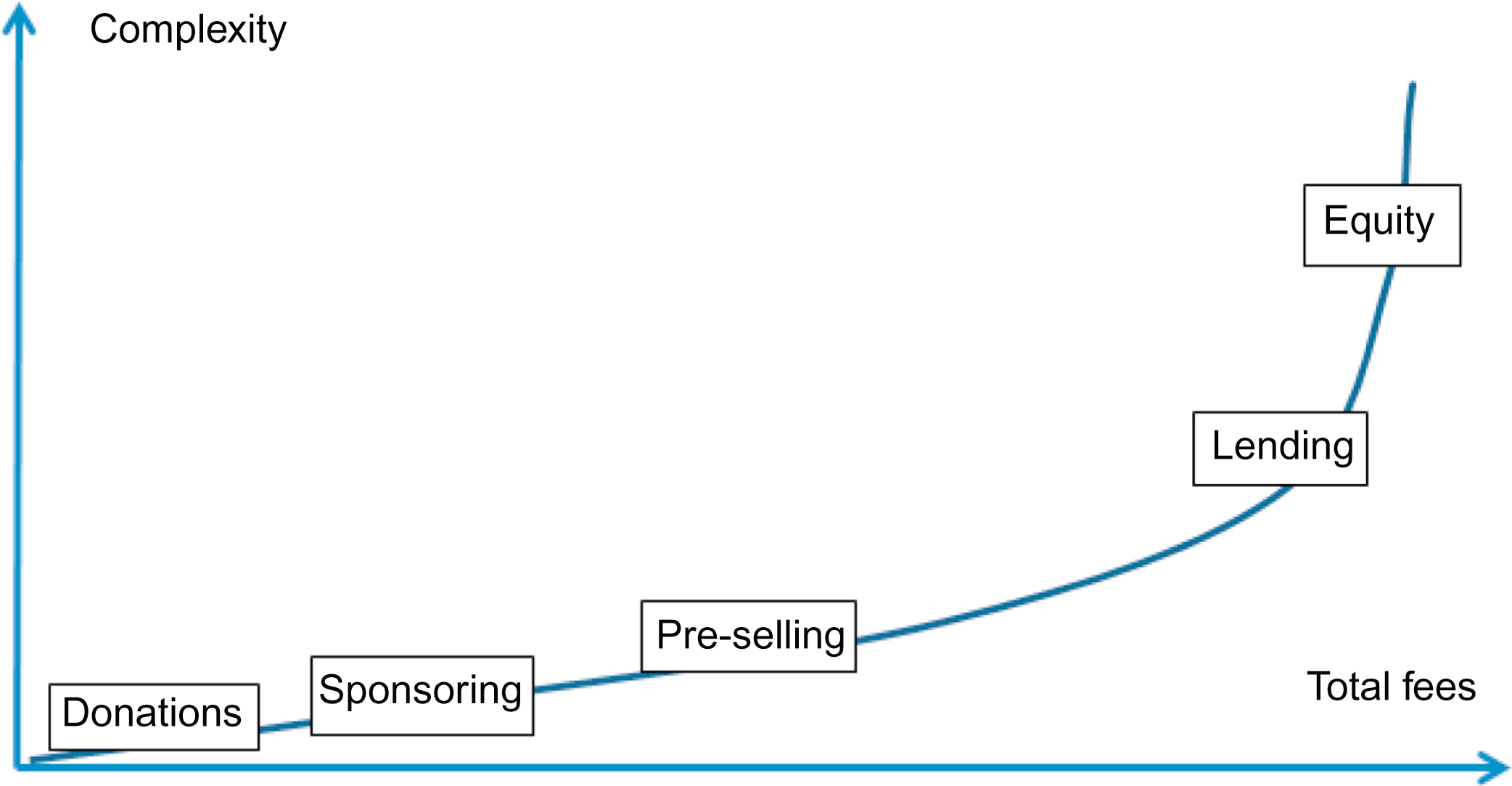

Figure 1 shows that the complexity of transactions can vary a lot, depending on the chosen form. In order to highlight the differences between the different forms, Hemer (2011) suggests establishing specific terms for (crowd) donations, (crowd) sponsoring, (crowd) pre-ordering or pre-selling or (crowd) lending and (crowd) investments.

Most crowdfunding platforms have three properties in common:

They provide initiators with a standardized and comprehensive presentation format for their project, accessible to anyone with Internet access.

They allow small to medium-sized financial transactions that enable widespread participation and keep risks within reasonable limits.

They provide information on the investments (such as the cumulative amount raised to date and the online identity of current investors), as well as communication tools enabling investors and potential investors to communicate with each other.

All platforms operate under the same principle of gathering together small investments from the crowd in order to fund a project that requires a large investment. Some platforms even go further, offering services such as giving advice, organizing public relations or making arrangements with micro-payment providers. Thus, crowdfunding platforms share the experience and professionalism they have developed through their routine work with project initiators who usually go through the crowdfunding process only once or no more than a few times in their lifetime. As such, all actors involved in crowdfunding processes are beneficiaries: initiators should be able to raise more funds, supporters should profit from better projects and rewards and platforms should get more traffic and so, make more money. In the usual business model of crowdfunding, platforms receive a given percentage of the funded money as a compensation for the service provided. Hemer (2011) underlined the importance and role of these platforms: ‘The rapid emergence of such platforms is logical and crucial for this new market to be able to function properly’. Crowdfunding platforms also set up the rules concerning the kinds of projects accepted; they therefore in some sense assume the role of gatekeepers. Users sometimes perceive platform guidelines as too restrictive and unclear; also policies vary from one platform to another. IndieGoGo for example is one of the least regulated online crowdfunding platforms. The co-founder of IndieGoGo, Slava Rubin, thinks that this openness is essential: ‘Some other players out there decide whether or not your project deserves to be on there and we think that this fundamentally goes against the reason the Internet was created and how to best use an Internet platform. The whole point of the Internet is to allow for it to be supply of demand, democratic determination of what deserves to be funded’ (in Bell, 2010). Kickstarter, on the other hand, represents a platform that is well known for its restrictive guidelines, and even if lay out is not always consistent, potential backers are sure of finding projects of a certain quality on the platform.

In the last couple of years a variety of different crowdfunding platforms have emerged on the market; they offer a wide range of services that specialize in different sorts of activities: music and films, charity projects or raising venture capital for start-ups. Three types of crowdfunding platforms can be identified:

Platforms characterized by high levels of risk/return with predominantly material payoffs for consumers. This model is close to venture capitalism;

Platforms characterized by a low-to-medium risk/return ratio with a broader set of potential payoffs for customers, including emotional rewards;

Platforms with little or no risk for customers who expect only non-material payoff. This model is close to charitable activities.

As seen above, platforms are generally classified according to the type of return funders will receive. The Crowdfunding Industry Report (2012) distinguishes four different types of crowdfunding platform: equity-based, lending-based, reward-based and finally donation-based crowdfunding.

Donation-Based Model and Reward-Based Model

The donation-based model is probably the simplest type of all crowdfunding models: the crowd gives money or other resources because they want to support a cause. The main difference between this model and the others is that there is no reward or compensation for the ‘investor’. The crowd gives money and gets nothing in return.

Reward-based crowdfunding happens when backers make donations for a project with the expectation of a certain reward. The reward can be either material (the backer will often be rewarded with the product itself if the funding is successful. It thus corresponds to a pre-ordered product or immaterial. Presently, most crowdfunding platforms follow this reward based model and such platforms show a high growth rate for example in 2012, their growth rate was close to 80%. Moreover, reward-based crowdfunding models can be split into two sub-categories: The ‘all or nothing’ model and the ‘keep what you raise’ model:

The main characteristic of the ‘all or nothing’ model is the compulsory objective of raising the targeted sum of money within a period of time set in advance. If the funding is not raised within that timeframe, the fundraising is unsuccessful and no money will change hands. In this scenario the pledged amounts will be transferred back to the pledger or simply stay in the pledger’s bank account. This model protects backers against unsuccessful projects because money is only transferred when the amount required to realize the full project is raised successfully. Project initiators may also benefit from the practice, as potential supporters are more likely to contribute to projects with unclear outcome knowing that the full project must be funded in order to be realized. Project fundraising often exceeds the original funding goal. Kickstarter is the most popular example of the ‘All or Nothing’ model, as it only pays out successfully funded projects.

In the ‘keep what you raise’ model, the raised funds are paid to the project initiators, regardless of whether or not the project reaches its funding goal by the end of the chosen timeframe. Thus, the ‘Keep what you raise’ model does not provide the security of the ‘All or nothing’ model. IndieGoGo is one of the most popular examples of this category of platforms. The majority of these crowdfunding platforms have established incentives in order to motivate initiators to reach their funding goals. For example, if project founders reach or exceed their funding goals, they benefit from services such as lower submission fees.

Equity-Based Model

Sellaband, one of the first crowdfunding platforms, introduced the equity-based crowdfunding model to a wide public. This particular model of crowdfunding allows any Internet in the world to invest small amounts of money in projects with a share in ownership of the project proportional to the investment in return. This model is equivalent to buying company stocks without any intermediaries. According to the Crowdfunding Industry Report (2012), equity-based crowdfunding is the fastest-growing category and is a model particularly suitable for digital goods, such as applications (‘apps’) or computer games, films, music and literature. This category also raises the largest sums of money per campaign. In 2012, 42% of the campaigns in this category raised above $100,000. The ability to raise large sums of money makes equity-based crowdfunding a great funding alternative to present funding sources. Small businesses and start-ups that always find it difficult to raise the necessary funds, could benefit highly from this new source of funding. However, in many countries, legislation makes equity crowdfunding difficult. Legal procedures for equity crowdfunding are usually more complicated than for current funding sources and make equity-based crowdfunding impossible for smaller projects. However, some crowdfunding platforms have found ways to get round the existing rules. George Castrataro, an American attorney, has identified two methods, the club model and the cooperative model:

In the club model, backers become members of a private ‘investment club’. This means that the offer is not made directly to the public (but to an ‘investment club’) and so the transaction is not illegal.

The cooperative model is organized on a similar basis as the club model above. The platform creates a cooperative vehicle to collect individual contributions and pool them into many single legal entities. Then, the various legal entities invest in the projects on the platform.

Microfinance or Lending-Based Models

Microfinance is still an emerging concept in the world of finance that has only recently expanded to the online world. The term stands for a broad category of financial services that are mainly provided to the poor and the underprivileged. Lawyers believe that microfinance platforms could empower those on low-incomes who do not usually qualify for bank loans and will help such people achieve positive returns that lift them out of poverty. The best-known example of micro financing via the Internet is Kiva, an online micro-lending platform that allows Internet users to offer small loans to people in need. Prosper is another such platform but it focuses more on the business aspect of lending. The concept cuts out the middleman and connects people who need money with people who have it; borrowers get better rates and investors better returns on their loans. We can distinguish two sub-categories, micro lending and peer-to-peer lending:

Micro lending means granting financial services, particularly microloans, to low-income clients who usually do not have access to banking and related services. The capital is pooled from the crowd and managed by a platform.

Peer-to-peer lending corresponds to individuals lending and borrowing money directly from each other without any intermediary. Platforms like Prosper and Zopa act as an interface by setting the rules and connecting borrowers and lenders directly. To reduce the risk, lenders usually contribute to only a small share of the funds needed by a borrower.

Table 1 sums up the different models and characteristics of crowdfunding used on platforms.

Crowdfunding Models.

| Crowdfunding Category | Mechanism | Explanation |

|---|---|---|

| Donation-based model | Donation | Funds are raised for non-profit organizations, for example, platforms for charity organizations |

| Reward-based model | All or nothing | If the targeted funds are raised, funds are transferred to project founder, otherwise the transaction is cancelled |

| Take it all | The project founder will receive the raised funds, even if the amount is inferior to the displayed objective for the full project | |

| Lending-based model | Peer-to-peer | Peer to peer collected loans providing interest or no interest at all |

| Micro-lending | Micro-credit | |

| Equity-based model | Cooperative model | Cooperative investment organization in exchange for an equity stake |

| Club model | Equivalent to a private ‘investment club’ |

After detailing the different aspects of crowdfunding in the first part of this chapter, we now focus on analyzing recent academic literature in this growing research area.

Chronological and Qualitative Analysis of Academic Literature on Crowdfunding

We found 97 referenced published academic articles in the studied databases. We performed bibliometrics on these articles in order to comprehend the nature and content of published articles on crowdfunding. The first publications came out in 2011 and we studied publications up to January 2015. During this period, we studied the relevant publications according to four major disciplines: Finance, Law (regulation), Management and Marketing.

Table 2 recapitulates publications per year on crowdfunding. The growth of rate of publications is similar to that of crowdfunding itself. Indeed, more than half of the academic articles were published in 2014 and around half of these were was in the field of finance.

Summary of Publications per Year.

| Years | Articles | Finance | Law (Regulation) | Management | Marketing | |

|---|---|---|---|---|---|---|

| 2011 | 4 | 4% | 3 | 1 | ||

| 2012 | 10 | 10% | 6 | 1 | 2 | 1 |

| 2013 | 28 | 29% | 13 | 3 | 8 | 3 |

| 2014 | 49 | 51% | 25 | 6 | 13 | 5 |

| 2015 | 6 | 6% | 2 | 4 | ||

| Total | 49 | 10 | 28 | 9 | ||

| % | 49 | 10 | 29 | 10 | ||

The highest number of articles on crowdfunding appear in the Venture Capital journal: seven articles in total, including a special issue in 2013 and two articles in 2014. Two journals published four articles: Strategic Change in 2014 and Entrepreneurship, Theory and Practice in 2015. Two other journals published three articles each, the Journal of Business Venturing in 2014 and the CPA Journal in 2013 and 2014. In addition, 10 journals published two articles each between 2012 and 2015: Strategic Finance, Research Technology Management, Procedia-Social and Behavioral Sciences, the International Journal of Arts Management, the International Financial Law Review, Financial Executive, Economics Letters, the Delaware Journal of Corporate Law, the Business Strategy Review and Business Horizons. Finally, 56 articles appeared in different journals as single publications.

Until 2011, crowdfunding literature was mainly provided by scattered non-academic media or through working papers. Scientific production really started after that date. Our analysis focuses on this consolidation period that is 2011–2015.

Regarding the quality of the academic journals, 19 journals are ranked in the French CNRS ranking system (Centre National de Recherche Scientifique) in section 37, ‘Economics and Management’: seven journals are ranked 1 (highest rank), three journals are ranked 2, four journals are ranked 3 and five journals are ranked 4 (lowest rank). Table 3 summarizes the 19 different journals concerned. We also took account of the ABS (Chartered Association of Business Schools) ranking where 4 correspond to the highest level.

Quality of Journals with Published Academic Articles on Crowdfunding.

| French CNRS Ranking | International ABS Ranking | Name of Journal | Number of Academic Published Articles |

|---|---|---|---|

| 1 | 4 | Entrepreneurship: Theory & Practice | 4 articles in 2015 |

| 4 | Journal of Business Venturing | 3 articles in 2014 | |

| 4 | Journal of Marketing Research | 1 article in 2011 | |

| 4 | Management Science | 1 article in 2013 | |

| 4 | Information Systems Research | 1 article in 2013 | |

| 4 | Organization Science | 1 article in 2014 | |

| 4 | MIS Quarterly | 1 article in 2014 | |

| 2 | 3 | Marketing Letters | 1 article in 2014 |

| 3 | Journal of Economic Behavior and Organization | 1 article in 2014 | |

| 3 | Information & Management | 1 article in 2014 | |

| 3 | 2 | Strategic Change | 4 articles in 2014 and 2015 |

| 3 | Economics Letters | 2 articles in 2014 | |

| 2 | Journal of Economic Issues | 1 article in 2013 | |

| 3 | Entrepreneurship & Regional Development | 1 article in 2014 | |

| 4 | ns | International Journal of Arts Management | 2 articles in 2014 |

| 2 | Journal of Service Management | 1 article in 2013 | |

| ns | Revue Management et Avenir | 1 article in 2014 | |

| ns | Revue Française de Gestion | 1 article in 2014 | |

| ns | 2 | Society and Business Review | 1 article in 2015 |

Institutional Analysis of Contributors on Crowdfunding Literature

Analysis of the Main Academic Authors on Crowdfunding

Among the authors on crowdfunding, many are professionals and not academics, three professionals work for the U.S. Securities and Exchange Commission. Most of the professionals work for Finance or Law consulting firms.

The most published author is Armin Schwienbacher, from Lille Nord de France University and SKEMA Business School. He published four articles, as early as 2012; the first publication was in a book, the three others were written in 2013 and 2014 with co-authors Paul Belleflamme and Thomas Lambert, both from Louvain University in Belgium. Two other authors, Anindya Ghose from New York University and Othmar Lehner from Oxford University, stand out with three publications each. Both authors have two publications in 2014 and one in 2013. These dates (2013 and 2014) show that the most productive authors got interested in the phenomenon of crowdfunding very early on.

Several authors have published two articles on crowdfunding:

- –

Two authors are from American Universities: Gordon Burtch from Minnesota University and Sunil Wattal from Pennsylvania University, each of them with one article published in 2013 and one in 2014,

- –

Two authors are from English Universities: Gary Dushnitsky from the London Business School published two articles in 2013 and Stéphanie Macht from Northumbria University two articles in 2014,

- –

Two co-authors come from a Lithuanian University Kaunas University of Technology: Sima Jegeleviciute and Loreta Valanciene, have one publication in 2013 and one in 2014,

- –

Avi Goldfarb from Toronto University in Canada was published twice in 2014 and Cristina Rossi-Lamastra from the Italian Politecnico di Milano published one article in 2013 and one in 2015.

Table 4 summarizes the above information.

Top Publishing Authors on Crowdfunding.

| Authors | Number of Articles | University | Year of Publication |

|---|---|---|---|

| Schwienbacher, Armin | 4 | Lille Nord, France University and SKEMA Business School, France | 2 articles in 2014 |

| 1 article in 2013 and in 2012 | |||

| Belleflamme, Paul | 3 | Catholic University Louvain, Belgium and CESifo, Munich, Germany | 2 articles in 2014 |

| 1 article in 2013 | |||

| Lambert, Thomas | 3 | Catholic University Louvain, Belgium | 2 articles in 2014 |

| 1 article in 2013 | |||

| Ghose, Anindya | 3 | New York University/Korea University Business School | 2 articles in 2014 |

| 1 article in 2013 | |||

| Lehner, Othmar | 3 | Oxford University, UK | 2 articles in 2014 |

| 1 article in 2013 | |||

| Burtch, Gordon | 2 | Minnesota Carlson School of Management, USA | 1 article in 2014 and in 2013 |

| Dushnitsky, Gary | 2 | London Business School, UK | 2 articles in 2013 |

| Goldfarb, Avi | 2 | Toronto University, Canada | 2 articles in 2014 |

| Jegeleviciute, Sima | 2 | Kaunas University of Technology, Lithuania | 1 article in 2014 and in 2013 |

| Macht, Stephanie | 2 | Northumbria University, UK | 2 articles in 2014 |

| Rossi-Lamastra, Cristina | 2 | Politecnico di Milano, Italy | 1 article in 2015 and in 2013 |

| Valanciene, Loreta | 2 | Kaunas University of Technology, Lithuania | 1 article in 2014 and in 2013 |

| Wattal, Sunil | 2 | Temple University, Philadelphia, Pennsylvania | 1 article in 2014 and in 2013 |

It is important to notice that many contributors of crowdfunding have not yet published in academic journals, although they are frequently cited in literature reviews. This implies that that crowdfunding research is still developing and on the way to consolidation.

Academic Institutions Showing an Interest in Crowdfunding

Two universities, among the top list of Universities identified as those with the highest numbers of articles published on crowdfunding, display six publications or occurrences. First, the Catholic University of Louvain in Belgium with the authors Paul Belleflamme and Thomas Lambert. And then Kaunas University of Technology in Lithuania.

Three Universities follow with five identified occurrences: Edinburgh University in the UK, HEC Montréal in Québec, Canada and the Politecnico di Milano in Italy. In the top five of the publishing Universities, there is a clear predominance from European authors studying crowdfunding. Among Universities having four identified occurrences, Europe is still outstanding with the University Lille Nord de France and SKEMA Business School and the publications of Armin Schwienbacher. Publications from different authors also show that Simon Fraser University in Toronto has five occurrences. US Universities appear three times: New York University has four occurrences; Delaware State University and Oklahoma State University each have three occurrences. One Chinese University, the Southwestern University, has three occurrences. Other Universities having three occurrences are European: three Universities are located in the UK (London Business School, Northumbria University and Oxford University), one is located in Italy (Bocconi University), one is French (Burgundy School of Business), one is German (Johannes Kepler Universitat), one is Belgian (Vrije Universiteit Brussel) and finally, one University, Toronto University, is Canadian.

Looking at the number of occurrences per University in Table 5, the European predominance is clear. However, if we study a larger sample of academic publications, American publications on crowdfunding can be pointed out. Thus, publications on crowdfunding are largely American with 50 occurrences, in other words, more than half of all publications on crowdfunding. UK publications come second with 19 occurrences, and Canadian publications come third with 16 occurrences. Germany, France and Italy each have 11 occurrences. Last, Belgium has nine occurrences. We do not mention other countries as the number of publications per country is small (Table 6).

Top Publishing Universities on Crowdfunding.

| Number of Occurrences | University | Country |

|---|---|---|

| 6 | Catholic University Louvain | Belgium |

| 6 | Kaunas University of Technology | Lithuania |

| 5 | Edinburgh University | UK |

| 5 | HEC Montréal | Canada |

| 5 | Politecnico di Milano | Italy |

| 4 | Simon Fraser University, University of Toronto | Canada |

| 4 | Université Lille Nord de France and SKEMA Business School | France |

| 4 | New York University | The United States |

| 3 | Bocconi University | Italy |

| 3 | Burgundy School of Business | France |

| 3 | Delaware State University | The United States |

| 3 | Johannes Kepler Universitat | Austria |

| 3 | London Business School | UK |

| 3 | Northumbria University | UK |

| 3 | Oklahoma State University | The United States |

| 3 | Oxford University | UK |

| 3 | Southwestern University | China |

| 3 | Toronto University | Canada |

| 3 | Vrije Universiteit Brussel | Belgium |

Top Publishing Countries on Crowdfunding.

| Countries | Number of Occurrences |

|---|---|

| United States | 50 |

| United Kingdom | 19 |

| Canada | 16 |

| France | 11 |

| Italy | 11 |

| Belgium | 9 |

| Germany | 8 |

Thematic Research on Crowdfunding

After a period of significant scatter, scientific production on crowdfunding has begun a process of consolidation. Together with this stabilized and focused growth, major topics and methods are emerging from the literature and following clear avenues for research whereas other sides of the crowdfunding question remain poorly explored.

Present Theory on Crowdfunding: Mainly Positive and Outcome-Oriented

Out of the 29 articles published in ranked reviews (Table 3), 19 follow the objectives of positive research, that is they describe and identify causalities in crowdfunding practices. The access to huge databases provided by platforms may play a major role in this orientation. Only seven papers adopt normative approaches, whereas such approaches constituted most of the academic and above all non-academic contributions in the early years of crowdfunding (up to 2011). Finally, only three articles analyse crowdfunding practices critically.

The subjects of research are also quite focused. They mainly deal with the behaviour of backers (11 articles, very few investigate the behaviour of entrepreneurs) and the factors that have an impact on the success of crowdfunding campaigns (eight articles). Behavioural studies focus on social and geographical distance as determinants of backers’ intention to subscribe. Scattered contributions examine the impact of other factors like rewards, or the behaviour of backers as a crowd through herding phenomena. Factors of success are considered from various perspectives, including mostly backer selection, communication (signalling and or narratives), and social capital. Normative papers promote methods for organizing campaigns, communicating, and building a trust relationship with backers.

After almost 10 years of experiencing crowdfunding, very few critical papers are proposed. Some of these provide an assessment of crowdfunding experiences, whereas others try to understand how ‘online crowds’ can still be ‘crowds’.

In such a context, the fact that 19 articles out of 29 are based on quantitative methodologies does not sound counterintuitive.

Emerging Questions on Crowdfunding and the Need for Additional Theory

Academic literature on crowdfunding is developing but currently it provides only partial knowledge of the social, legal, psychological and managerial challenges of crowdfunding practices. In the non-academic field, there are more and more descriptive inquiries, more or less justified recommendations are accumulating (with lots of ‘How to’ books), but crowdfunding remains a fuzzy subject for research and reflexivity. The need for theory on crowdfunding is three-fold if it is to address both scholars and practitioners:

A need for additional positive theory. Crowdpreneurs, crowdfunders and researchers are committed to understanding how crowdfunding projects are organized, how (and why) they may succeed or fail and how governments consider this new practice and try to regulate it.

A need for normative theory. Crowdpreneurs and crowdfunders may need templates and ‘recipes’ for developing (or to assessing and taking part in) projects. However, beyond this basic knowledge, they also need to know which models are more efficient and how to legitimate their actions.

A need for critical theory. To make crowdfunding more sustainable than just a managerial fad, reflexivity must be developed on its social and economic impact. If regulation and practice have to be oriented in one specific direction which one should it be?

Conclusion

Our cartography of academic literature on crowdfunding has highlighted the youth of this literature that starting only in 2011, and its rapid expansion since then. We highlighted the fact that most of the publications are from the Finance field, that is to say half of publications over the studied years are Finance related, followed by publications coming from the field of Management field (one third of total publications) and then publications from the domains of Marketing and Law. The cartography has also highlighted a handful of very prolific and mainly European authors on crowdfunding. Similarly, the top publishing Universities are also European. However, interestingly, by far the top publishing country is the United States. Followed by the United Kingdom and Canada, but with far fewer publications, this book includes authors and practices from the United States, the United Kingdom and Europe but also from Africa, Brazil and India. This book also wishes to address issues not only from a financial but also from a social, legal and economic focus. Part One defends the need for positive theory. Crowdpreneurs, crowdfunders and researchers are committed to understanding how crowdfunding projects are organized, how (and why) they may succeed or fail, how governments consider this new practice and try to regulate it. Part Two defends the need for normative theory. Crowdpreneurs and crowdfunders may need templates and ‘recipes’ for developing (or to assessing and taking part in) projects. But beyond this basic knowledge, they should know which models are more efficient or how to legitimate their action. Lastly, Part Three supports the need for critical theory. To make crowdfunding more sustainable than just a managerial fad, reflexivity must be developed on its social and economic impact. If regulation and practice have to be oriented in one specific direction which one should it be?

Karima Bouaiss

Isabelle Maque

Jérôme Méric

DATABASE FOR ANALYSIS

Agrawal, Catalini, & Goldfarb (2011) Agrawal, A. , Catalini, C. , & Goldfarb, A. (2011). The geography of crowdfunding. Working Paper, NET Institute Working Paper Series No. 16820. Ahlers, Cumming, Günther, & Schweizer (2015) Ahlers, G. K. C. , Cumming, D. , Günther, C. , & Schweizer, D. (2015). Signaling in equity crowdfunding. Entrepreneurship Theory and Practice, 39(4), 955–988. Allison, Davis, Short, & Webb (2015) Allison, T. H. , Davis, B. C. , Short, J. C. , & Webb, J. W. (2015). Crowdfunding in a prosocial microlending environment: Examining the role of intrinsic versus extrinsic cues. Entrepreneurship Theory and Practice, 39(1), 53–73. Baker & Bulkley (2014) Baker, W. E. , & Bulkley, N. (2014). Paying it forward vs. Rewarding reputation: Mechanisms of generalized reciprocity. Organization science, 25(5), 1493–1510. Belleflamme, Lambert, & Schwienbacher (2014) Belleflamme, P. , Lambert, T. , & Schwienbacher, A. (2014). Crowdfunding: Tapping the right crowd. Journal of Business Venturing, 29(5), 585–609. Bessière & Stéphany (2014) Bessière, V. , & Stéphany, E. (2014). Le financement par crowdfunding: Quelles spécificités pour l’évaluation des entreprises? Revue Française de Gestion, 40-242, 149–161. Boeuf, Darveau, & Legoux (2014) Boeuf, B. , Darveau, J. , & Legoux, R. (2014). Financing creativity: Crowdfunding as a new approach for theatre projects. International Journal of Arts Management, 16(3), 33–44. Bouaiss, Maque, & Méric (2015) Bouaiss, K. , Maque, I. , & Méric, J. (2015). More than three’s a crowd … in the best interest of companies!: Crowdfunding as Zeitgeist or ideology? Society and Business Review, 10(1), 23–39. Bruton, Khavul, Siegel, & Wright (2015) Bruton, G. , Khavul, S. , Siegel, D. , & Wright, M. (2015). New Financial alternatives in seeding entrepreneurship: Microfinance, crowdfunding, and peer-to-peer innovations. Entrepreneurship Theory and Practice, 39(1), 9–26. Burtch, Ghose, & Wattal (2013) Burtch, G. , Ghose, A. , & Wattal, S. (2013). An empirical examination of the antecedents and consequences of contribution patterns in crowd-funded markets. Information Systems Research, 24(3), 499–519. Burtch, Ghose, & Wattal (2014) Burtch, G. , Ghose, A. , & Wattal, S. (2014). Cultural differences and geography as determinants of online prosocial lending. MIS Quarterly, 38(3), 773–794. Cholakova & Clarysse (2015) Cholakova, M. , & Clarysse, B. (2015). Does the possibility to make equity investments in crowdfunding projects crowd out reward-based investments? Entrepreneurship Theory and Practice, 39(1), 145–172. Colombo, Franzoni, & Rossi-Lamastra (2015) Colombo, M. G. , Franzoni, C. , & Rossi-Lamastra, C. (2015). Internal social capital and the attraction of early contributions in crowdfunding. Entrepreneurship Theory and Practice, 39(1), 75–100. Dushnitsky & Marom (2014) Dushnitsky, G. , & Marom, D. (2014). Crowd monogamy. Business Strategy Review, 24(4), 24–26. Galak, Small, & Stephen (2011) Galak, J. , Small, D. , & Stephen, A. T. (2011). Microfinance decision making: A field study of prosocial lending. Journal of Marketing Research, 48(Special issue), S130–S137. Lambrecht et al. (2014) Lambrecht, A. , Goldfarb, A. , Bonatti, A. , Ghose, A. , Goldstein, D. G. , Lewis, R. , … Yao, S. (2014). How do firms make money selling digital goods online? Marketing Letters, 25(3), 331–341. Larivière et al. (2013) Larivière, B. , Joosten, H. , Malthouse, E. C. , van Birgelen, M. , Aksoy, P. , Kunz, W. H. , & Huang, M.-H. (2013). Value fusion: The blending of consumer and firm value in the distinct context of mobile technologies and social media. Journal of Service Management, 24(3), 268–293. Lehner (2014) Lehner, O. M. (2014). The formation and interplay of social capital in crowdfunded social ventures. Entrepreneurship & Regional Development, 26(5–6), 478–499. Macht (2014) Macht, S. A. (2014). Reaping value-added benefits from crowdfunders: What can we learn from relationship marketing? Strategic Change, 23(7–8), 439–460. Macht & Weatherston (2014) Macht, S. A. , & Weatherston, J. (2014). The benefits of online crowdfunding for fund-seeking business ventures. Strategic Change, 23(1–2), 1–14. Macht & Weatherston (2015) Macht, S. A. , & Weatherston, J. (2015). Academic research on crowdfunders: What’s been done and what’s to come? Strategic Change, 24(2), 191–205. Meer (2014) Meer, J. (2014). Effects of the price of charitable giving: Evidence from an online crowdfunding platform. Journal of Economic Behavior & Organization, 103(July), 113–124. Mollick (2014) Mollick, E. (2014). The dynamics of crowdfunding: An exploratory study. Journal of Business Venturing, 29(1), 1–16. Moss, Neubaum, & Meyskens (2015) Moss, T. W. , Neubaum, D. O. , & Meyskens, M. (2015). The effect of virtuous and entrepreneurial orientations on microfinance lending and repayment: A signaling theory perspective. Entrepreneurship Theory and Practice, 39(1), 27–52. Onnée & Renault (2014) Onnée, S. , & Renault, S. (2014). Crowdfunding: vers une compréhension du rôle joué par la foule. Management & Avenir, 74(8), 117–133. Parker (2014) Parker, S. C. (2014). Crowdfunding, cascades and informed investors. Economics Letters, 125(3), 432–435. Pitschner & Pitschner-Finn (2014) Pitschner, S. , & Pitschner-Finn, S. (2014). Non-profit differentials in crowd-based financing: Evidence from 50,000 campaigns. Economics Letters, 123(3), 391–394. Royal, Sampath, & Windsor (2014) Royal, C. , Sampath, G. , & Windsor, S. (2014). Microfinance, crowdfunding, and sustainability: A case study of telecenters in a South Asian developing country. Strategic Change, 23(7–8), 425–438. Sahm, Belleflamme, Lambert, & Schwienbacher (2014) Sahm, M. , Belleflamme, P. , Lambert, T. , & Schwienbacher, A. (2014). Corrigendum to “Crowdfunding: Tapping the right crowd”. Journal of Business Venturing, 29(5), 610–611. Stockenstrand & Owe (2014) Stockenstrand, A. K. , & Owe, A. (2014). Arts funding and its effects on strategy, management and learning. International Journal of Arts Management, 17(1), 43–53. Valanciene & Jegeleviciute (2013) Valanciene, L. , & Jegeleviciute, S. (2013). Valuation of crowdfunding, benefits and drawbacks. Economics and Management, 18(1), 39–48. Van Staveren (2013) Van Staveren, I. (2013). Caring finance practices. Journal of Economic Issues, 47(2), 419–425. Zhang & Peng (2012) Zhang, J. , & Peng, L. (2012). Rational herding in microloan markets. Management Science, 58(5), 892–912. Zheng, Li, Wu, & Xu (2014) Zheng, H. , Li, D. , Wu, J. , & Xu, Y. (2014). The role of multidimensional social capital in crowdfunding: A comparative study in China and US. Information & Management, 51(4), 488–496.ADDITIONAL REFERENCES

Bell (2010) Bell, M. (2010). Wake me up before you IndieGoGo: Interview with Slava Rubin. Film Threat. Retrieved from http://www.filmthreat.com/interviews/26476/. Accessed on October 5, 2010. Castrataro (2012) Castrataro, D. (2012). Crowdfunding platforms: To each their own. Retrieved from http://socialmediaweek.org/blog/2012/01/crowdfunding-platforms-to-each-their-own/ Hemer (2011) Hemer, H. (2011). A snapshot on crowdfunding (p. 43). Karlsruhe: Fraunhofer ISI. No. R2/2011.INTERNET SOURCES

Crowdfunding Industry Report (2012) Crowdfunding Industry Report . (2012). crowdsourcing.org, May. Retrieved from http://www.crowdfunding.nl/wp-content/uploads/2012/05/92834651-Massolution-abridged-Crowd-Funding-Industry-Report1.pdfNote

Source: Wardrop, Robert, Bryan Zhang, Raghavendra Rau and Mia Gray (2015). “Moving Mainstream: The European Alternative Finance Benchmarking Report”, University of Cambridge and EY. Available at: http://www.jbs.cam.ac.uk/fileadmin/user_upload/research/centres/alternative-finance/downloads/2015-uk-alternative-finance-benchmarking-report.pdf

- Prelims

- Part One Positive Crowdfunding Theory – Micro Economic Underpinnings, Contingency Factors and Regulation Issues

- Chapter 1 An Industrial Organization Framework to Understand the Strategies of Crowdfunding Platforms

- Chapter 2 Equity Crowdfunding in Africa: How Can Investment Micro-Behaviors Make the Crowdfunding Macro-System Work?

- Chapter 3 Crowdfunding: How and Why People Participate

- Chapter 4 Crowdfunding for Social Enterprises: An Exploratory Analysis of the Italian Context

- Chapter 5 Crowdfunding Legal Framework: An International Analysis

- Part Two Normative Crowdfunding Theory – Models, Modes and Contexts

- Chapter 6 Creating Project Legitimacy – The Role of Entrepreneurial Narrative in Reward-Based Crowdfunding

- Chapter 7 Crowdlending as a Socially Innovative Corporate Financial Instrument

- Chapter 8 A Social Network Approach for Crowdfunding

- Chapter 9 The Investment Model of Crowdfunding for MSME (Micro, Small and Medium Enterprises) in India

- Chapter 10 Is Crowdfunding Sharia Compliant?

- Part Three Critical Crowdfunding Theory – Social, Legal and Economic Impacts

- Chapter 11 Crowdfunding in Present Society: Deconstructing the Zeitgeist

- Chapter 12 Equity-Based Crowdfunding: Allowing the Masses to Take a Slice of the Pie

- Chapter 13 Crowdfunding Seen through the Lens of the Psychological Contract

- About the Authors

- Index